Top 4 Tax Efficient Retirement Strategies in the US

Identify four key tax-efficient strategies for retirement planning in the US to minimize taxes and maximize savings.

Identify four key tax-efficient strategies for retirement planning in the US to minimize taxes and maximize savings. Planning for retirement in the US can feel like navigating a maze, especially when you factor in taxes. Nobody wants to work hard their whole life only to see a big chunk of their retirement savings disappear to Uncle Sam. That's why understanding tax-efficient retirement strategies is super important. It's not just about saving money; it's about saving it smartly so it grows more and lasts longer. We're going to dive into some of the best ways to keep more of your hard-earned cash in your pocket during your golden years. Think of this as your friendly guide to making your retirement fund work harder for you, not for the taxman.

Top 4 Tax Efficient Retirement Strategies in the US

Understanding Tax Advantaged Retirement Accounts The Foundation of Smart Saving

When we talk about tax-efficient retirement strategies, the first thing that usually comes to mind are tax-advantaged accounts. These aren't just fancy names; they're powerful tools designed by the government to encourage you to save for retirement by offering some sweet tax breaks. The two big players here are 401(k)s and IRAs, and they come in two main flavors: traditional and Roth. Each has its own set of rules and benefits, and choosing the right one (or a combination) can significantly impact your tax bill both now and in retirement.

Traditional 401(k) and IRA Pre-Tax Contributions and Deferred Growth

Let's start with the traditional accounts. When you contribute to a traditional 401(k) or IRA, your contributions are typically made with pre-tax dollars. This means the money you put in reduces your taxable income for the year you contribute. So, if you earn $70,000 and contribute $6,000 to a traditional 401(k), your taxable income drops to $64,000. That's an immediate tax saving! The money then grows tax-deferred, meaning you don't pay taxes on any investment gains until you withdraw the money in retirement. This deferral allows your money to compound more aggressively over time, as you're not losing a chunk to taxes each year. However, the catch is that when you do withdraw the money in retirement, both your contributions and earnings are taxed as ordinary income. This strategy is often great if you expect to be in a lower tax bracket in retirement than you are now.

For example, let's say you're in your 30s, earning a good salary, and in a 24% tax bracket. Contributing to a traditional 401(k) or IRA means you save 24 cents on every dollar you contribute right now. If you expect your income to drop significantly in retirement, perhaps because you're no longer working or have fewer expenses, then paying taxes at a lower rate later makes a lot of sense.

Roth 401(k) and IRA After-Tax Contributions and Tax-Free Withdrawals

Now, let's flip the coin to Roth accounts. With a Roth 401(k) or IRA, you contribute money that you've already paid taxes on (after-tax dollars). The big advantage here is that your money grows tax-free, and when you take qualified withdrawals in retirement, they are completely tax-free. Yes, you read that right – completely tax-free! This is a huge benefit, especially if you expect to be in a higher tax bracket in retirement than you are today, or if you simply want the peace of mind knowing your retirement income won't be subject to future tax rate increases.

Roth accounts are particularly appealing to younger individuals who are likely in lower tax brackets now but anticipate earning more and being in higher tax brackets later in their careers. It's also a fantastic option if you're just starting out and your income is relatively low. Paying taxes on that money now, at a lower rate, can save you a fortune in taxes down the road. There are income limitations for contributing directly to a Roth IRA, but the 'backdoor Roth' strategy can often bypass these for higher earners. Roth 401(k)s, however, don't have income limits for contributions.

Comparing Traditional vs Roth Which One is Right for You

Choosing between traditional and Roth often boils down to your current and projected future tax brackets. If you think your tax bracket will be lower in retirement, traditional accounts might be better. If you think it will be higher, Roth accounts are likely the winner. Many people also choose to diversify by contributing to both, getting a mix of upfront tax deductions and future tax-free income. This 'tax diversification' can be a very smart move, giving you flexibility no matter what future tax laws bring.

For instance, if your employer offers a Roth 401(k) and you're in a moderate tax bracket, contributing to it could be a great way to lock in tax-free growth. If you're a high earner, you might max out your traditional 401(k) for the immediate tax deduction, and then use the backdoor Roth IRA strategy to get some tax-free growth as well. It's all about balancing your current tax situation with your future financial goals.

Maximizing Employer Sponsored Plans 401(k)s and 403(b)s

Employer-sponsored retirement plans like 401(k)s (for for-profit companies) and 403(b)s (for non-profit organizations and schools) are often the first and best place to start your tax-efficient retirement savings journey. These plans offer some incredible advantages that individual IRAs don't always provide, especially when it comes to contribution limits and employer matching.

Employer Match Free Money for Your Future

One of the biggest perks of employer-sponsored plans is the employer match. Many companies will contribute a certain amount to your 401(k) or 403(b) based on how much you contribute. For example, an employer might match 50 cents on the dollar for the first 6% of your salary you contribute. This is essentially free money! Not taking advantage of an employer match is like turning down a raise. It's an immediate, guaranteed return on your investment, and it's tax-deferred (or tax-free if it's a Roth match, though that's less common). Always contribute at least enough to get the full employer match – it's the easiest way to boost your retirement savings.

Let's say your salary is $80,000 and your employer matches 50% of your contributions up to 6% of your salary. If you contribute 6% ($4,800), your employer will contribute an additional $2,400. That's an instant 50% return on your $4,800, before any investment growth! This is a no-brainer for building wealth.

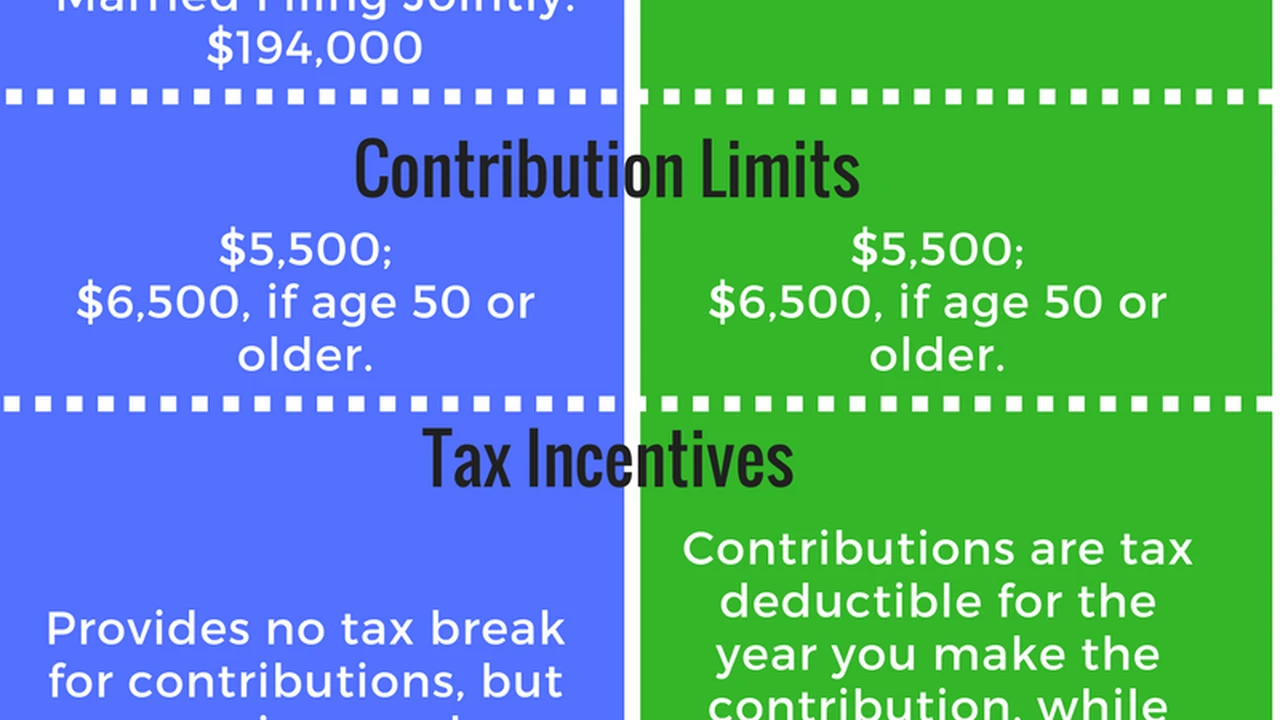

High Contribution Limits More Room to Grow

Another significant advantage of 401(k)s and 403(b)s is their higher contribution limits compared to IRAs. For 2024, you can contribute up to $23,000 to a 401(k) or 403(b), with an additional catch-up contribution of $7,500 if you're age 50 or older. This is substantially more than the $7,000 (or $8,000 for age 50+) limit for IRAs. These higher limits allow you to shelter a much larger portion of your income from taxes, either now (traditional) or in the future (Roth).

Maximizing these contributions, especially if you're a high earner, can significantly reduce your current taxable income and accelerate your retirement savings. It's a powerful way to supercharge your wealth building while enjoying immediate tax benefits.

Accessing Funds Before Retirement The Rule of 55

While generally you face penalties for withdrawing from retirement accounts before age 59½, employer-sponsored plans offer a special rule: the 'Rule of 55.' If you leave your job (whether voluntarily or involuntarily) in the year you turn 55 or later, you can withdraw funds from that employer's 401(k) or 403(b) without incurring the 10% early withdrawal penalty. This can be a huge advantage for those who plan to retire earlier than 59½, providing a bridge to other retirement income sources or until they reach the standard withdrawal age. It's a niche but powerful tax-efficient strategy for early retirees.

Health Savings Accounts HSAs The Triple Tax Advantage Powerhouse

When it comes to tax-efficient retirement strategies, the Health Savings Account (HSA) is often overlooked, but it's truly a powerhouse. It's sometimes called the 'triple tax advantage' account, and for good reason. HSAs are available to individuals enrolled in a high-deductible health plan (HDHP), and if you qualify, you should absolutely consider contributing to one.

Triple Tax Advantage Explained

1. Tax-Deductible Contributions: Like a traditional IRA, your contributions to an HSA are tax-deductible. This means they reduce your taxable income for the year you contribute, saving you money on your current tax bill.

2. Tax-Free Growth: The money in your HSA grows tax-free. You don't pay taxes on any interest, dividends, or capital gains generated by your investments within the account.

3. Tax-Free Withdrawals for Qualified Medical Expenses: This is the real kicker. If you use the money for qualified medical expenses (which are plentiful and often increase in retirement), your withdrawals are completely tax-free. This includes everything from doctor visits and prescriptions to dental care and even Medicare premiums in retirement.

No other account offers this triple tax benefit. It's like a Roth account for medical expenses, but with an upfront tax deduction too!

Using Your HSA as a Retirement Investment Vehicle

While HSAs are designed for healthcare costs, many savvy investors use them as an additional retirement investment vehicle. The strategy is to pay for current medical expenses out-of-pocket (if you can afford to) and let the money in your HSA grow untouched for as long as possible. You can invest the funds within your HSA, just like a 401(k) or IRA, allowing them to compound over decades.

In retirement, you can then withdraw the money tax-free for medical expenses. And here's another cool trick: you can reimburse yourself for past qualified medical expenses that you paid out-of-pocket, as long as you kept the receipts. This means you could have a large sum of money growing tax-free for years, and then effectively withdraw it tax-free for any purpose by matching it to old medical receipts.

If you reach retirement and have more HSA funds than you need for medical expenses, after age 65, you can withdraw money for any purpose without penalty, though it will be taxed as ordinary income (similar to a traditional IRA). So, it acts as a backup retirement account even if you don't have medical expenses.

HSA Providers and Investment Options

Many financial institutions offer HSAs, and the investment options can vary. Some popular HSA providers that offer good investment choices include:

* Fidelity HSA: Fidelity is a well-known brokerage with a wide range of investment options, including low-cost ETFs and mutual funds. They generally have no monthly maintenance fees if you meet certain balance requirements or have an active brokerage account. Their investment platform is robust, making it a great choice for those who want to actively manage their HSA investments.

* Lively HSA: Lively partners with TD Ameritrade (now Schwab) for investments, offering a broad selection of ETFs and mutual funds. They are known for their user-friendly platform and transparent fee structure. They often have no monthly fees for individuals, making them very attractive.

* HealthEquity: HealthEquity is one of the largest HSA administrators. They offer a range of investment options, though sometimes with slightly higher fees or more limited choices compared to pure brokerages. They are often the default provider if your employer offers an HSA.

* Optum Bank: Another large HSA provider, Optum Bank offers various investment options, often through a partnership with a brokerage firm. Their fee structure can vary, so it's important to check the details.

When choosing an HSA provider, consider the fees (monthly maintenance, investment fees), the range of investment options (ETFs, mutual funds, individual stocks), and the user-friendliness of their platform. For example, if you're comfortable with self-directed investing, Fidelity or Lively might be excellent choices due to their broad investment selection and competitive fees. If your employer offers an HSA, compare its features with independent providers to see if you're getting the best deal.

Tax Loss Harvesting and Asset Location Advanced Strategies for Investors

Once you've maxed out your tax-advantaged accounts, or if you have additional money to invest, you'll likely be investing in a taxable brokerage account. Here, two advanced tax-efficient strategies come into play: tax-loss harvesting and asset location. These can help you minimize taxes on your investment gains and maximize your after-tax returns.

Tax Loss Harvesting Turning Losses into Tax Savings

Tax-loss harvesting involves selling investments at a loss to offset capital gains and, potentially, a limited amount of ordinary income. Here's how it works: if you have investments that have gone down in value, you can sell them, realize the loss, and then use that loss to offset any capital gains you've realized from selling other investments at a profit. If your capital losses exceed your capital gains, you can use up to $3,000 of those losses to offset your ordinary income each year. Any remaining losses can be carried forward indefinitely to offset future gains or income.

This strategy doesn't mean you're giving up on the investment. You can immediately reinvest the proceeds into a similar (but not 'substantially identical' to avoid the wash-sale rule) investment to maintain your market exposure. For example, if you sell an S&P 500 index fund at a loss, you could immediately buy a different S&P 500 index fund from a different provider or an ETF that tracks the same index. This allows you to capture the tax benefit without significantly altering your investment strategy.

Tax-loss harvesting is particularly effective in volatile markets, as it creates more opportunities to realize losses. Many robo-advisors, like Betterment and Wealthfront, automate tax-loss harvesting for their clients, making it easy to implement this strategy without constant manual intervention. For example, if you invest $10,000 in an S&P 500 ETF and it drops to $9,000, you could sell it, realize a $1,000 loss, and immediately buy a different S&P 500 ETF. That $1,000 loss can then offset other gains or reduce your taxable income.

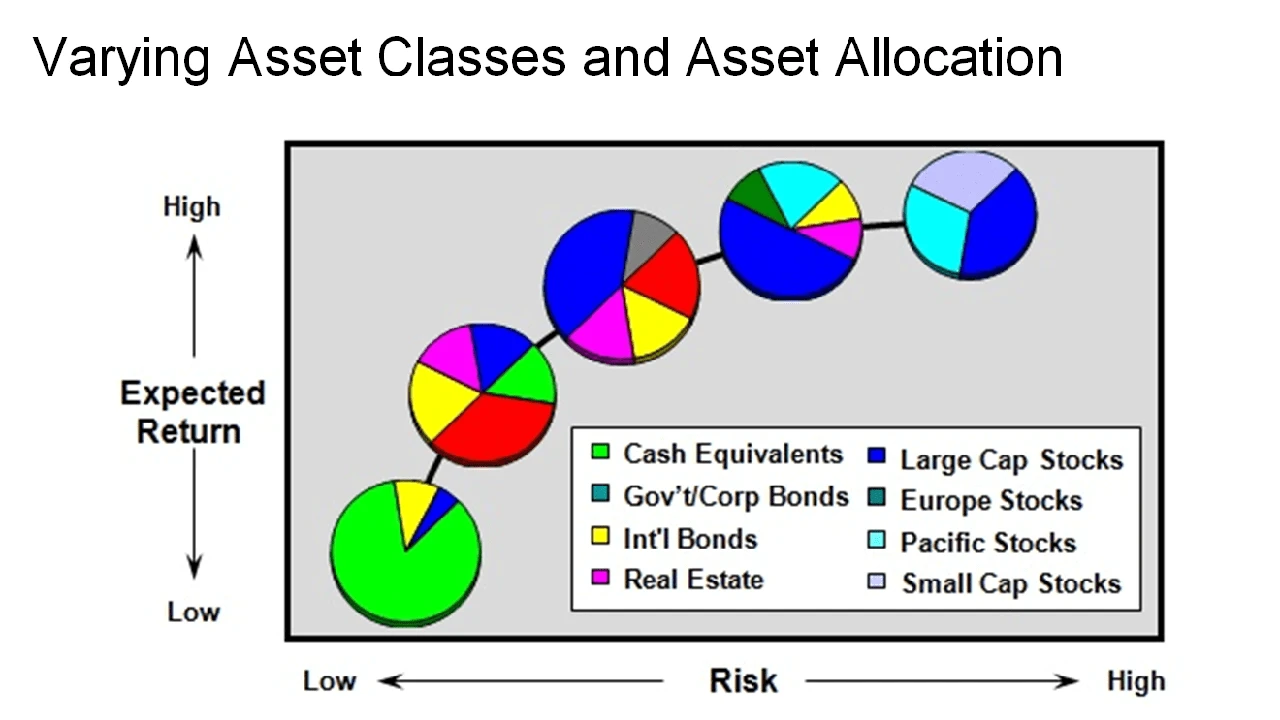

Asset Location Placing Investments in the Right Accounts

Asset location is about strategically placing different types of investments into different types of accounts (taxable, tax-deferred, tax-free) to minimize your overall tax burden. The general rule of thumb is to put investments that generate a lot of ordinary income (like bonds, REITs, or actively managed funds with high turnover) into tax-deferred accounts (like traditional 401(k)s or IRAs). This way, you defer paying taxes on that income until retirement, allowing it to compound more efficiently.

Conversely, investments that generate qualified dividends or long-term capital gains (like broad-market index funds or individual stocks you plan to hold for a long time) are often best placed in taxable brokerage accounts. This is because qualified dividends and long-term capital gains are taxed at lower rates than ordinary income. If you put these in a Roth account, they'd be tax-free, which is even better, but if you've maxed out your Roth options, a taxable account is the next best place.

For example, if you have a traditional 401(k), a Roth IRA, and a taxable brokerage account:

* Traditional 401(k): Consider placing high-income-generating assets like corporate bonds, REITs, or high-dividend stocks here. The income they generate will be tax-deferred.

* Roth IRA: This is the ideal place for your highest-growth potential assets, like aggressive growth stocks or small-cap funds, because all future growth and withdrawals will be tax-free.

* Taxable Brokerage Account: Place broad-market index funds (like VOO or SPY) or individual stocks you plan to hold for the long term here. Their qualified dividends and long-term capital gains will be taxed at favorable rates.

This strategy helps you optimize your tax situation across your entire portfolio, rather than just focusing on individual accounts. It's a bit more complex to manage, but the tax savings over decades can be substantial.

Robo-Advisors for Automated Tax Efficiency

For those who want to implement these advanced strategies without the manual effort, robo-advisors can be a fantastic solution. Platforms like Betterment and Wealthfront are designed with tax efficiency in mind. They automatically handle things like tax-loss harvesting, asset location, and rebalancing, often at a lower cost than traditional financial advisors.

* Betterment: Known for its automated tax-loss harvesting, Betterment also implements asset location strategies. They offer diversified portfolios of low-cost ETFs. Their annual advisory fee is typically 0.25% of assets under management for balances under $100,000, and it decreases for higher balances. They also offer a premium tier with access to human advisors.

* Wealthfront: Similar to Betterment, Wealthfront provides automated tax-loss harvesting and asset location. They also offer 'direct indexing' for larger accounts, which can provide even more tax-loss harvesting opportunities. Their annual advisory fee is also typically 0.25% of assets under management.

These services are great for investors who want a hands-off approach to tax-efficient investing. They continuously monitor your portfolio for opportunities to reduce your tax bill, which can add significant value over the long term, especially in taxable accounts.

Conclusion

Navigating the world of retirement planning in the US can be complex, but by understanding and implementing these tax-efficient strategies, you can significantly boost your savings and ensure more of your money works for you. From leveraging tax-advantaged accounts like 401(k)s, IRAs, and HSAs, to employing advanced techniques like tax-loss harvesting and asset location, there are numerous ways to minimize your tax burden. Remember, the key is to start early, contribute consistently, and regularly review your strategy to adapt to life changes and evolving tax laws. By being proactive and smart about your retirement planning, you can build a robust financial future and enjoy your golden years with greater peace of mind.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)