Comparing Traditional IRA vs Roth IRA for US Retirement

Understand the differences between Traditional IRA and Roth IRA to choose the best retirement account for your US financial situation.

Understand the differences between Traditional IRA and Roth IRA to choose the best retirement account for your US financial situation.

Comparing Traditional IRA vs Roth IRA for US Retirement

Hey there, future retiree! Navigating the world of retirement accounts can feel a bit like trying to read a foreign language, especially when you're faced with acronyms like IRA. But don't sweat it! Today, we're going to break down two of the most popular Individual Retirement Arrangements (IRAs) for folks in the US: the Traditional IRA and the Roth IRA. We'll dive deep into what makes them tick, who they're best for, and even look at some real-world scenarios to help you figure out which one (or maybe even both!) fits your financial puzzle best. Think of this as your friendly guide to making smart choices for your golden years.

Traditional IRA Unpacking the Basics and Benefits

Let's kick things off with the Traditional IRA. This has been a go-to retirement savings vehicle for decades, and for good reason. It offers some pretty sweet tax advantages, especially if you expect to be in a lower tax bracket in retirement than you are now. So, what's the deal?

How a Traditional IRA Works Contributions and Deductions

When you contribute to a Traditional IRA, your contributions might be tax-deductible. This means the money you put in reduces your taxable income for the year you contribute. Imagine you earn $70,000 and contribute $6,000 to a Traditional IRA. Your taxable income could drop to $64,000, potentially saving you a good chunk of change on your current tax bill. The exact deductibility depends on a few factors, like whether you (or your spouse) are covered by a retirement plan at work and your Modified Adjusted Gross Income (MAGI).

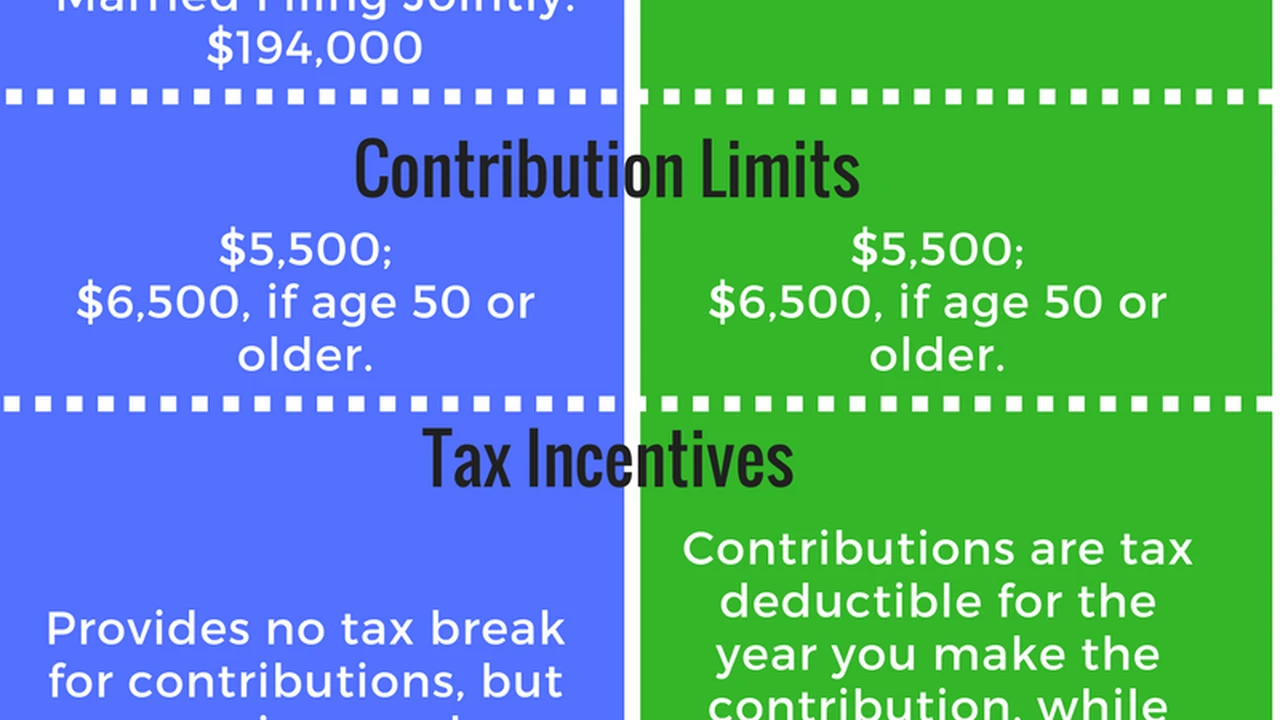

For 2024, the maximum you can contribute to an IRA (Traditional or Roth, combined) is $7,000, or $8,000 if you're age 50 or older. These limits are set by the IRS and can change, so it's always a good idea to double-check the latest figures.

Tax Deferred Growth Understanding the Power of Compounding

One of the biggest perks of a Traditional IRA is tax-deferred growth. This means your investments grow and compound over time without being taxed annually. You won't pay taxes on any earnings until you start taking withdrawals in retirement. This can be a huge advantage, as it allows your money to grow faster because you're not losing a portion of your gains to taxes each year. It's like planting a money tree and letting it grow without anyone picking the fruit until you're ready to harvest.

Withdrawals in Retirement When and How You Pay Taxes

Once you hit age 59½, you can start taking qualified withdrawals from your Traditional IRA without penalty. These withdrawals, both your original contributions and any earnings, will be taxed as ordinary income at your then-current tax rate. If you withdraw money before 59½, you'll generally face a 10% early withdrawal penalty, plus the withdrawals will be taxed as ordinary income. There are a few exceptions to this rule, such as for certain medical expenses, higher education costs, or a first-time home purchase (up to $10,000).

Who Benefits Most from a Traditional IRA Ideal Scenarios

A Traditional IRA is often a fantastic choice for individuals who:

- Expect to be in a lower tax bracket in retirement: If you're earning a good income now and anticipate a lower income (and thus lower tax bracket) when you retire, the upfront tax deduction can be very valuable.

- Want to reduce their current taxable income: The tax deduction can help lower your current tax bill, freeing up more money for other financial goals.

- Are not eligible for Roth IRA contributions due to high income: If your income exceeds the limits for contributing directly to a Roth IRA, a Traditional IRA (and potentially a backdoor Roth conversion, which we'll touch on later) might be your best bet.

Roth IRA Decoding the Tax Free Future

Now, let's shift gears to the Roth IRA, the younger sibling of the Traditional IRA, but with a very different tax philosophy. The Roth IRA is all about tax-free withdrawals in retirement, which can be incredibly powerful.

How a Roth IRA Works After Tax Contributions

Unlike the Traditional IRA, contributions to a Roth IRA are made with after-tax dollars. This means you don't get an upfront tax deduction for the money you put in. So, if you contribute $6,000 to a Roth IRA, your taxable income for the year remains unchanged. The contribution limits are the same as for a Traditional IRA: $7,000 for 2024, or $8,000 if you're 50 or older.

Tax Free Growth and Withdrawals The Ultimate Perk

Here's where the Roth IRA truly shines: your investments grow tax-free, and qualified withdrawals in retirement are also completely tax-free. Yes, you read that right – no taxes on your earnings when you take them out! To qualify for tax-free withdrawals, two conditions must be met: you must be at least 59½ years old, and your Roth IRA must have been open for at least five years (this is known as the five-year rule).

Contribution Income Limits Understanding the MAGI Thresholds

One important thing to note about Roth IRAs is that there are income limitations for direct contributions. For 2024, if your Modified Adjusted Gross Income (MAGI) is above certain thresholds, you might not be able to contribute the full amount, or any amount, to a Roth IRA. For example, if you're a single filer, the ability to contribute starts to phase out at a MAGI of $146,000 and is completely phased out at $161,000. These limits are adjusted annually, so always check the latest IRS guidelines.

Who Benefits Most from a Roth IRA Ideal Scenarios

A Roth IRA is often an excellent choice for individuals who:

- Expect to be in a higher tax bracket in retirement: If you're currently in a lower tax bracket and anticipate earning more (or tax rates increasing) in the future, paying taxes on your contributions now can save you a lot in the long run.

- Value tax-free income in retirement: Knowing that your retirement withdrawals will be completely tax-free provides incredible peace of mind and predictability.

- Are younger and have a long time horizon for their investments: The longer your money has to grow tax-free, the more powerful the Roth IRA becomes.

- Want more flexibility with withdrawals: You can withdraw your Roth IRA contributions (not earnings) at any time, tax-free and penalty-free, for any reason. This can act as a sort of emergency fund, though it's generally not recommended to dip into retirement savings.

Traditional vs Roth IRA A Side by Side Comparison for US Investors

Let's put them head-to-head to make the differences crystal clear. This table summarizes the key distinctions:

| Feature | Traditional IRA | Roth IRA |

|---|---|---|

| Contribution Tax Treatment | Potentially tax-deductible (pre-tax) | Not tax-deductible (after-tax) |

| Growth Tax Treatment | Tax-deferred | Tax-free |

| Withdrawal Tax Treatment (Qualified) | Taxed as ordinary income | Tax-free |

| Income Limits for Contributions | No income limits for contributions, but deductibility may be limited based on MAGI and workplace plan coverage. | Yes, MAGI limits apply for direct contributions. |

| Required Minimum Distributions (RMDs) | Yes, generally starting at age 73 (or 75 for those turning 74 after 2032). | No RMDs for the original owner. |

| Early Withdrawal Penalties | 10% penalty + ordinary income tax (with exceptions) | 10% penalty on earnings (contributions can be withdrawn tax/penalty-free) |

Choosing Your IRA The Decision Making Process for US Savers

So, how do you decide which one is right for you? It really boils down to your current financial situation, your income, and your expectations for the future. Here are some common scenarios and considerations:

Scenario 1 High Current Income Lower Expected Retirement Income

If you're currently in a high tax bracket and expect your income to be lower in retirement (maybe you'll be living off a pension, Social Security, and your savings), a Traditional IRA might be your best bet. The upfront tax deduction can save you a significant amount of money now, and you'll pay taxes on withdrawals when you're in a lower tax bracket.

Scenario 2 Lower Current Income Higher Expected Retirement Income

If you're just starting your career, or you're in a relatively low tax bracket now, but you anticipate earning more and being in a higher tax bracket in retirement, a Roth IRA is often the winner. Paying taxes on your contributions now means all your growth and withdrawals in retirement are tax-free, which can be a massive advantage over decades of compounding.

Scenario 3 Unsure About Future Tax Brackets Flexibility is Key

If you're genuinely unsure about whether your tax bracket will be higher or lower in retirement, or if you just want to hedge your bets, consider contributing to both! Many financial advisors recommend a diversified approach, having both pre-tax (Traditional IRA/401k) and after-tax (Roth IRA/Roth 401k) money in retirement. This gives you flexibility to choose which accounts to draw from in retirement based on your tax situation at that time.

Scenario 4 High Income Earners The Backdoor Roth IRA Strategy

What if your income is too high to contribute directly to a Roth IRA? Don't despair! There's a popular strategy called the "backdoor Roth IRA." This involves contributing non-deductible money to a Traditional IRA and then immediately converting it to a Roth IRA. While the conversion itself might be taxable if you have pre-tax money in other Traditional IRAs (this is known as the pro-rata rule), it's a perfectly legal way for high-income earners to get money into a Roth IRA. It's a bit more complex, so if this sounds like you, definitely chat with a financial advisor.

Beyond IRAs Complementary Retirement Accounts for US Savers

While Traditional and Roth IRAs are fantastic, they're often just one piece of the retirement puzzle. Many people also utilize employer-sponsored plans and other investment vehicles. Let's quickly touch on a few:

401k and Roth 401k Maximizing Employer Sponsored Plans

If your employer offers a 401k (or 403b, TSP, etc.), especially one with an employer match, that should generally be your first priority. An employer match is essentially free money! Many 401k plans now also offer a Roth 401k option, which works similarly to a Roth IRA but with much higher contribution limits. For 2024, the 401k contribution limit is $23,000, or $30,500 if you're 50 or older.

Health Savings Accounts HSAs The Triple Tax Advantage

If you're enrolled in a high-deductible health plan (HDHP), you might be eligible for a Health Savings Account (HSA). HSAs are often called the "triple tax advantage" account because contributions are tax-deductible, growth is tax-free, and qualified withdrawals for medical expenses are also tax-free. If you don't use the money for medical expenses in retirement, it functions much like a Traditional IRA, with withdrawals taxed as ordinary income. It's a powerful tool for both healthcare and retirement savings.

Practical Application Choosing the Right Investment Platform

Once you've decided between a Traditional or Roth IRA, the next step is to open an account and start investing! You'll need to choose a brokerage firm or financial institution. Here are a few popular options in the US, along with some general insights:

Fidelity Investments A Comprehensive Platform

Fidelity is a giant in the investment world, offering a wide range of investment products, from mutual funds and ETFs to individual stocks and bonds. They have a strong reputation for customer service and offer extensive educational resources. Their platform is user-friendly for both beginners and experienced investors. They offer both Traditional and Roth IRAs. Fidelity is known for its low-cost index funds and ETFs, making it a great choice for cost-conscious investors. They also have physical branches if you prefer in-person assistance. Pricing: Many commission-free ETFs and stocks, low expense ratios on their own funds. Use Case: Investors looking for a broad selection of investment options, strong research tools, and good customer support.

Vanguard Low Cost Index Fund Leader

Vanguard is famous for its low-cost index funds and ETFs, which are designed to track market performance with minimal fees. If you're a fan of passive investing and want to keep costs down, Vanguard is an excellent choice for your IRA. They also offer both Traditional and Roth IRAs. Their platform is straightforward, though perhaps not as flashy as some others. Pricing: Extremely low expense ratios on their index funds and ETFs, commission-free trading for Vanguard ETFs. Use Case: Cost-conscious investors, those who prefer passive investing strategies, and long-term buy-and-hold investors.

Charles Schwab A Blend of Value and Service

Charles Schwab is another top-tier brokerage firm that offers a great balance of low costs, a wide array of investment choices, and excellent customer service. They have a robust trading platform, extensive research, and a network of physical branches. They also offer both Traditional and Roth IRAs. Schwab has been very competitive with fees, often matching or beating competitors. Pricing: Commission-free stocks and ETFs, low-cost Schwab-branded index funds. Use Case: Investors who want a full-service brokerage experience with competitive pricing and strong research capabilities.

M1 Finance Automated Investing with Custom Portfolios

M1 Finance is a bit different. It's a hybrid platform that combines automated investing with the ability to create custom portfolios (they call them "Pies"). You choose your investments, and M1 automatically rebalances your portfolio to maintain your desired asset allocation. This can be great for hands-off investors who still want some control over their holdings. They offer both Traditional and Roth IRAs. Pricing: No management fees for basic accounts, commission-free trading. Use Case: Investors who want automated portfolio management with customization, and those who prefer a more modern, app-centric experience.

Fidelity Go and Schwab Intelligent Portfolios Robo Advisor Options

If you're looking for a completely hands-off approach, both Fidelity and Schwab offer robo-advisor services: Fidelity Go and Schwab Intelligent Portfolios. These services build and manage a diversified portfolio for you based on your risk tolerance and financial goals. They're great for beginners or those who prefer not to actively manage their investments. They can manage both Traditional and Roth IRAs for you. Pricing: Fidelity Go has a small advisory fee (e.g., 0.35% annually for balances over $25,000, no advisory fee for balances under $25,000). Schwab Intelligent Portfolios has no advisory fees for their basic service, but you'll be invested in Schwab ETFs. Use Case: Beginners, busy individuals, or anyone who wants professional portfolio management without the high cost of a traditional financial advisor.

Important Considerations for Your IRA Journey

Before you jump in, here are a few more things to keep in mind:

Contribution Limits Staying Within IRS Guidelines

Remember those contribution limits we talked about? They apply to the total amount you can contribute to all your IRAs (Traditional and Roth combined) in a given year. Don't over-contribute, as this can lead to penalties.

Investment Choices Diversification is Key

Once your money is in your IRA, you still need to invest it! Don't just let it sit in cash. Diversify your investments across different asset classes (stocks, bonds, real estate, etc.) to manage risk and maximize growth potential. Most brokerage firms offer a wide range of investment options within your IRA.

Beneficiary Designations Planning for the Unexpected

Always, always, always designate beneficiaries for your IRA. This ensures that your money goes to the people you intend it to, without having to go through probate. Keep your beneficiaries updated, especially after major life events like marriage, divorce, or the birth of a child.

Rollovers and Conversions Moving Your Money Wisely

You can roll over money from an old 401k into an IRA, or convert a Traditional IRA to a Roth IRA. These can be powerful strategies, but they have tax implications. For example, converting a Traditional IRA to a Roth IRA will generally be a taxable event, as you'll pay taxes on the pre-tax money being converted. Always understand the tax consequences before initiating a rollover or conversion.

Required Minimum Distributions RMDs for Traditional IRAs

For Traditional IRAs, you'll eventually have to start taking Required Minimum Distributions (RMDs) once you reach a certain age (currently 73, or 75 for those turning 74 after 2032). This is the IRS's way of making sure they eventually get their tax money. Roth IRAs, on the other hand, do not have RMDs for the original owner, which is another attractive feature for estate planning.

Wrapping It Up Your Retirement Future Awaits

Choosing between a Traditional IRA and a Roth IRA isn't about finding a single "best" option; it's about finding the best fit for your unique financial situation and future goals. Both are incredible tools for building a secure retirement, offering different tax advantages that can save you a lot of money over the long haul. Take the time to consider your current income, your expected retirement income, and your overall financial strategy. And remember, it's perfectly fine to use both, or to start with one and adjust as your circumstances change. The most important thing is to start saving and investing for your future today. Your future self will thank you!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)