Managing Risk in Your Investment Portfolio in the US

Practical strategies for US investors to effectively manage and mitigate risk within their investment portfolios.

Practical strategies for US investors to effectively manage and mitigate risk within their investment portfolios.

Managing Risk in Your Investment Portfolio in the US

Hey there, fellow investors! Let's talk about something super important when it comes to growing your money: managing risk. Nobody wants to see their hard-earned cash disappear, right? Especially in the US market, which can be a rollercoaster sometimes. So, whether you're just starting out or you've been in the game for a while, understanding how to protect your investments is key. It's not about avoiding all risk – that's pretty much impossible if you want to see any real growth – but it's about understanding it, measuring it, and taking smart steps to keep it in check. Think of it like driving a car; you can't avoid all hazards, but you can wear a seatbelt, drive defensively, and have good insurance. That's what we're aiming for with your portfolio.

We're going to dive deep into practical strategies that US investors can use to effectively manage and mitigate risk. We'll cover everything from diversification to understanding your own risk tolerance, and even look at some specific products and scenarios. So, buckle up, and let's get started on building a more resilient investment portfolio!

Understanding Investment Risk What Every US Investor Needs to Know

Before we can manage risk, we need to understand what it actually is. In the world of investing, risk generally refers to the possibility that your actual investment returns will differ from your expected returns. And usually, when we talk about risk, we're thinking about the potential for loss. But it's more nuanced than that. There are different types of risks, and they can affect your portfolio in various ways.

Market Risk The Big Picture for US Stocks and Bonds

This is often called systemic risk, and it's the risk that the entire market or a large segment of it will decline. Think about a major economic recession, a global pandemic, or a significant geopolitical event. These things can cause broad market downturns, affecting almost all investments, regardless of how well a particular company is doing. For US investors, this means that even if you've picked great companies, a market-wide slump can still hit your portfolio. You can't really diversify away from market risk entirely, but you can manage its impact.

Specific Risk Company and Industry Specific Factors

Also known as unsystematic risk, this is the risk associated with a specific company, industry, or asset. For example, a particular company might face a lawsuit, a product recall, or a change in consumer preferences that negatively impacts its stock price. Or an entire industry might be disrupted by new technology or regulations. This type of risk can be significantly reduced through diversification, which we'll talk about next.

Interest Rate Risk How Fed Decisions Impact Your US Investments

This risk primarily affects bond investments. When interest rates rise, the value of existing bonds (which pay a lower fixed interest rate) tends to fall. Conversely, when interest rates fall, existing bonds become more attractive, and their value tends to rise. For US investors holding bonds, especially longer-term ones, changes in the Federal Reserve's interest rate policy can have a noticeable impact.

Inflation Risk Protecting Your Purchasing Power in the US

Inflation is the rate at which the general level of prices for goods and services is rising, and consequently, the purchasing power of currency is falling. If your investments aren't growing at a rate that outpaces inflation, you're effectively losing money in real terms. This is a crucial risk for long-term investors in the US, as even a seemingly small inflation rate can significantly erode wealth over decades.

Liquidity Risk Accessing Your Funds When You Need Them

This is the risk that you won't be able to sell an investment quickly enough at a fair market price. Some investments, like real estate or certain private equity funds, are less liquid than publicly traded stocks or bonds. If you need to access your cash quickly, illiquid investments can pose a problem. For US investors, most publicly traded securities are highly liquid, but it's still something to be aware of, especially with alternative investments.

Diversification The Cornerstone of Risk Management for US Portfolios

Alright, let's get to the golden rule of investing: diversification. It's probably the most powerful tool you have to manage risk, especially specific risk. The old adage, 'Don't put all your eggs in one basket,' perfectly sums it up. By spreading your investments across different asset classes, industries, geographies, and types of securities, you reduce the impact that any single poor-performing investment can have on your overall portfolio.

Diversifying Across Asset Classes Stocks Bonds Real Estate and More

This is the first and most fundamental layer of diversification. Instead of putting all your money into stocks, consider allocating a portion to bonds, real estate, or even commodities. Different asset classes tend to perform differently under various economic conditions. For example, bonds often perform well when stocks are struggling, providing a cushion for your portfolio. A typical diversified US portfolio might include:

- Stocks: For growth potential.

- Bonds: For stability and income.

- Real Estate (REITs or direct ownership): For inflation hedge and income.

- Cash/Cash Equivalents: For liquidity and safety.

Geographic Diversification Investing Beyond the US Borders

While the US market is robust, relying solely on it exposes you to risks specific to the US economy. By investing in international markets, you can tap into growth opportunities elsewhere and reduce your exposure to any single country's economic downturns. For US investors, this means considering:

- Developed International Markets: Like Europe, Japan, Canada.

- Emerging Markets: Like China, India, Brazil, and many Southeast Asian countries.

You can achieve this through international mutual funds, ETFs, or even individual foreign stocks if you're adventurous.

Industry and Sector Diversification Spreading Your Bets in the US Economy

Even within the stock market, it's wise to diversify across different industries and sectors. Don't put all your money into tech stocks, for example, even if they've been performing well. If that sector takes a hit, your entire portfolio could suffer. Instead, spread your investments across:

- Technology

- Healthcare

- Financials

- Consumer Staples

- Energy

- Utilities

- And so on...

This way, if one sector experiences a downturn, others might be performing well, balancing out your returns.

Diversification by Company Size and Style Large Cap Small Cap Growth Value

Within the stock market, you can also diversify by company size (large-cap, mid-cap, small-cap) and investment style (growth vs. value). Large-cap companies tend to be more stable, while small-cap companies can offer higher growth potential but also higher risk. Growth stocks focus on companies expected to grow earnings at an above-average rate, while value stocks are typically undervalued companies. Combining these can lead to a more robust portfolio.

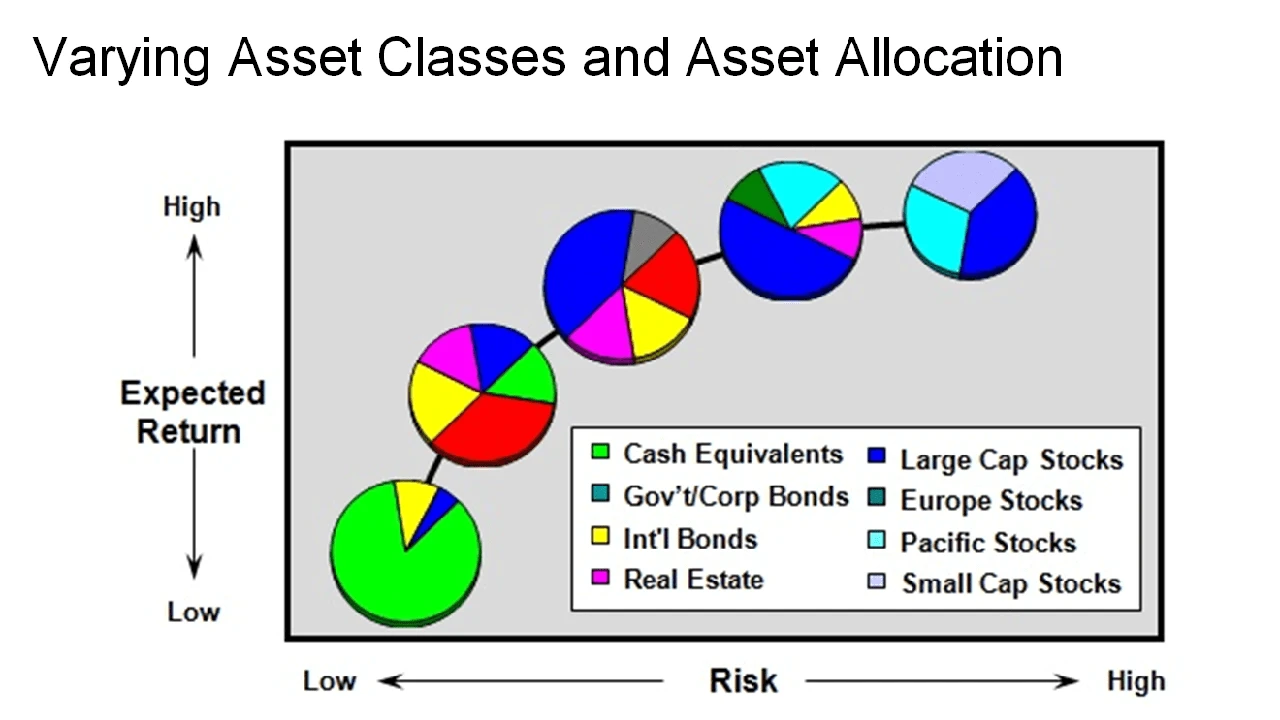

Asset Allocation Tailoring Your Portfolio to Your Risk Tolerance and Goals

Diversification is about spreading your investments, but asset allocation is about deciding how much to put into each asset class. This is a highly personal decision, as it depends on your individual risk tolerance, investment horizon, and financial goals. There's no one-size-fits-all answer here.

Determining Your Risk Tolerance How Much Volatility Can You Handle

This is perhaps the most critical step. Are you comfortable with significant fluctuations in your portfolio's value for the potential of higher returns? Or do you prefer a more stable, albeit potentially slower, growth path? Your risk tolerance is influenced by:

- Your age: Younger investors generally have a longer time horizon and can afford to take on more risk.

- Your financial situation: Do you have a stable income? An emergency fund?

- Your personality: How do you react to market downturns? Do you panic sell or see them as buying opportunities?

Many online tools and financial advisors can help you assess your risk tolerance.

Investment Horizon When Do You Need the Money

Your investment horizon is the length of time you plan to hold your investments. If you're saving for retirement 30 years away, you have a long horizon and can typically afford to take on more risk. If you need the money in 3-5 years for a down payment on a house, a shorter horizon suggests a more conservative approach.

Common Asset Allocation Models for US Investors

- Aggressive: High percentage in stocks (e.g., 80-90% stocks, 10-20% bonds). Suitable for young investors with a high-risk tolerance and long horizon.

- Moderate: Balanced approach (e.g., 60% stocks, 40% bonds). A common choice for many investors.

- Conservative: Higher percentage in bonds and cash (e.g., 30-40% stocks, 60-70% bonds/cash). Suitable for those nearing retirement or with a low-risk tolerance.

Remember, these are just guidelines. Your ideal allocation might be somewhere in between or even outside these ranges.

Risk Mitigation Strategies Beyond Diversification for US Investors

While diversification and asset allocation are foundational, there are other proactive steps you can take to manage risk in your US investment portfolio.

Dollar-Cost Averaging Smoothing Out Market Volatility

This strategy involves investing a fixed amount of money at regular intervals (e.g., monthly or quarterly), regardless of the market's performance. When prices are high, your fixed amount buys fewer shares; when prices are low, it buys more shares. Over time, this can average out your purchase price and reduce the impact of market volatility. It's a fantastic strategy for long-term investors, especially those contributing to 401(k)s or IRAs.

Rebalancing Your Portfolio Staying on Track

Over time, your initial asset allocation will drift as different investments perform better or worse. Rebalancing means periodically adjusting your portfolio back to your target asset allocation. For example, if stocks have performed exceptionally well, they might now represent a larger percentage of your portfolio than you initially intended. Rebalancing would involve selling some stocks and buying more bonds to get back to your desired ratio. This helps you maintain your desired risk level and forces you to 'buy low and sell high' (or at least 'sell high and buy low') in a disciplined way.

Stop-Loss Orders Limiting Your Downside on US Stocks

A stop-loss order is an instruction to your broker to sell a security if its price falls to a certain level. This can help limit your potential losses on individual stock holdings. For example, if you buy a stock at $100 and set a stop-loss at $90, your shares will be sold if the price drops to $90, preventing further losses. However, be aware that stop-loss orders don't guarantee a specific execution price, especially in fast-moving markets, and they can sometimes be triggered by temporary market fluctuations.

Hedging Strategies Advanced Risk Management for Sophisticated US Investors

Hedging involves taking an offsetting position in a related security to reduce the risk of adverse price movements. This is typically done using derivatives like options or futures. For example, an investor might buy put options on a stock they own to protect against a significant price drop. Hedging can be complex and is generally more suitable for experienced investors or those with very large portfolios, as it involves additional costs and can limit upside potential.

Specific Products and Tools for Risk Management in the US Market

Let's get practical and look at some specific products and tools that US investors can use to implement these risk management strategies.

Exchange Traded Funds ETFs for Diversification and Low Cost

ETFs are incredibly popular for diversification. They are funds that hold a basket of assets (like stocks, bonds, or commodities) and trade like individual stocks on an exchange. They offer instant diversification across various asset classes, sectors, and geographies, often with very low expense ratios.

Product Comparison: Popular Diversified ETFs for US Investors

- Vanguard Total Stock Market ETF (VTI): This ETF gives you exposure to the entire US stock market, from large-cap to small-cap companies. It's incredibly diversified within the US equity space.

- iShares Core S&P 500 ETF (IVV): Tracks the S&P 500, providing exposure to 500 of the largest US companies. A solid core holding for many.

- Vanguard Total International Stock ETF (VXUS): Offers broad exposure to non-US developed and emerging markets. Great for geographic diversification.

- Vanguard Total Bond Market ETF (BND): Provides exposure to the entire US investment-grade bond market, offering stability and income.

- Schwab US Dividend Equity ETF (SCHD): Focuses on high-quality, dividend-paying US companies, which can offer some downside protection during volatile times.

Usage Scenario: A moderate investor might allocate 60% to VTI, 30% to BND, and 10% to VXUS to achieve broad diversification across US and international stocks and US bonds. These ETFs typically have expense ratios ranging from 0.03% to 0.07%, making them very cost-effective.

Target-Date Funds Set It and Forget It Retirement Planning

These are mutual funds or ETFs that automatically adjust their asset allocation over time, becoming more conservative as you approach a specific target retirement date. They are designed to be a 'one-stop shop' for retirement savings, handling the rebalancing for you. They are excellent for investors who prefer a hands-off approach to asset allocation and risk management.

Product Comparison: Leading Target-Date Funds for US Retirement

- Vanguard Target Retirement Funds: Known for their low costs and broad diversification. They invest in a mix of Vanguard's underlying index funds.

- Fidelity Freedom Index Funds: Similar to Vanguard, these funds use Fidelity's index funds to create diversified portfolios that adjust over time.

- Schwab Target Index Funds: Another strong contender, offering low-cost, diversified target-date solutions.

Usage Scenario: A 30-year-old US investor planning to retire in 2060 might choose the Vanguard Target Retirement 2060 Fund. The fund will automatically shift from a higher stock allocation to a higher bond allocation as 2060 approaches. Expense ratios typically range from 0.08% to 0.15%.

Robo-Advisors Automated Portfolio Management and Risk Assessment

Robo-advisors are digital platforms that use algorithms to manage your investments based on your risk tolerance and financial goals. They typically build diversified portfolios using low-cost ETFs and automatically rebalance them. They're a great option for investors who want professional portfolio management without the high fees of a traditional financial advisor.

Product Comparison: Top Robo-Advisors for US Investors

- Betterment: Offers diversified portfolios, automatic rebalancing, tax-loss harvesting, and goal-based planning. Management fees typically range from 0.25% to 0.40% of assets under management (AUM).

- Wealthfront: Similar to Betterment, with a strong focus on tax-loss harvesting and sophisticated portfolio options. Management fees are generally 0.25% of AUM.

- Fidelity Go: A good option for existing Fidelity customers, offering automated investing with no advisory fees for balances under $25,000 and 0.35% for balances above that.

- Schwab Intelligent Portfolios: Offers commission-free automated investing with no advisory fees, though it does hold a cash allocation that doesn't earn interest.

Usage Scenario: A busy professional in the US who wants a diversified, automatically managed portfolio without spending much time on it could use Betterment. After answering a few questions about their risk tolerance, Betterment would construct and manage a suitable portfolio of ETFs. Minimums can be as low as $0 or $500, depending on the platform.

Fixed Income Products for Stability and Capital Preservation

Bonds and other fixed-income securities are crucial for risk management, especially for conservative investors or those nearing retirement. They provide stability, income, and can act as a hedge against stock market volatility.

Product Comparison: Key Fixed Income Options for US Investors

- US Treasury Bonds/Notes/Bills: Considered among the safest investments globally, backed by the full faith and credit of the US government. They offer varying maturities and are ideal for capital preservation. You can buy them directly from TreasuryDirect.gov or through brokers.

- Investment-Grade Corporate Bonds: Issued by financially strong companies, these offer higher yields than Treasuries but come with slightly more credit risk. You can access them through bond ETFs (like BND mentioned above) or individual bonds through a brokerage.

- Municipal Bonds (Munis): Issued by state and local governments, the interest earned on munis is often exempt from federal income tax, and sometimes state and local taxes too, making them attractive for high-income US investors. You can buy individual munis or muni bond ETFs.

- Certificates of Deposit (CDs): Offered by banks, CDs are FDIC-insured savings accounts that hold your money for a fixed period at a fixed interest rate. They offer guaranteed returns and capital preservation, though typically lower yields than bonds.

Usage Scenario: An investor looking to preserve capital and generate stable income for a portion of their portfolio might allocate funds to a mix of US Treasury bonds and a high-quality corporate bond ETF. For tax-advantaged income, a municipal bond fund could be considered. CDs are great for short-term savings goals where capital preservation is paramount.

Behavioral Finance and Risk Management Avoiding Common Pitfalls

Finally, let's talk about the biggest risk factor in your portfolio: yourself! Our emotions and cognitive biases can often lead us to make irrational investment decisions, especially during times of market stress. Understanding these behavioral pitfalls is a crucial part of risk management.

Emotional Investing Panic Selling and FOMO

When the market drops, the natural instinct for many is to panic and sell everything to stop the bleeding. This is often the worst thing you can do, as you lock in losses and miss out on the subsequent recovery. Conversely, during bull markets, 'Fear Of Missing Out' (FOMO) can lead investors to chase hot stocks or sectors, often buying at the peak. Stick to your plan, remember your long-term goals, and avoid making impulsive decisions based on fear or greed.

Confirmation Bias Seeking Information That Confirms Your Beliefs

We all tend to seek out information that confirms what we already believe and ignore information that contradicts it. In investing, this can lead to overconfidence in certain investments or a reluctance to admit when an investment isn't working out. Actively seek out diverse perspectives and challenge your own assumptions.

Overconfidence Thinking You Can Beat the Market

While it's good to be confident, overconfidence can lead to excessive risk-taking, insufficient diversification, and frequent trading (which often leads to higher costs and lower returns). Most individual investors are better off focusing on broad market diversification and long-term strategies rather than trying to pick individual winners or time the market.

Anchoring Focusing on Past Prices

Anchoring is when we rely too heavily on the first piece of information we receive (the 'anchor') when making decisions. For investors, this often means fixating on the price at which they bought a stock, rather than its current fundamentals or future prospects. Don't let past prices dictate your current decisions.

By being aware of these behavioral biases, you can take steps to counteract them. Having a well-defined investment plan, sticking to your asset allocation, and using automated tools like robo-advisors or target-date funds can help remove emotion from your decision-making process.

Managing risk in your investment portfolio isn't about eliminating risk entirely; it's about understanding it, measuring it, and taking calculated steps to protect your capital while still pursuing your financial goals. By implementing strategies like diversification, appropriate asset allocation, and leveraging smart products and tools, you can build a more resilient portfolio that can weather market storms and help you achieve long-term success in the US market. Stay disciplined, stay informed, and keep your emotions in check!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)