Comparing Zero Based Budgeting vs 50 30 20 Rule

Understand the differences between zero-based budgeting and the 50/30/20 rule to find the best budgeting method for your financial situation.

Understand the differences between zero-based budgeting and the 50/30/20 rule to find the best budgeting method for your financial situation. Choosing the right budgeting method can feel like navigating a financial maze. Two popular and highly effective strategies often come up in discussions: Zero-Based Budgeting (ZBB) and the 50/30/20 Rule. Both aim to help you manage your money better, but they approach the task from very different angles. So, which one is right for you? Let's dive deep into each method, compare their pros and cons, explore real-world applications, and even recommend some tools to help you get started.

Zero Based Budgeting vs 50 30 20 Rule A Comprehensive Guide

When it comes to personal finance, budgeting is your superpower. It's the roadmap that guides your money, ensuring you know where every dollar goes and that you're working towards your financial goals. But with so many budgeting philosophies out there, it's easy to get overwhelmed. Today, we're going to break down two of the most talked-about methods: Zero-Based Budgeting and the 50/30/20 Rule. By the end of this guide, you'll have a clear understanding of which approach might be your financial soulmate.

What is Zero Based Budgeting ZBB Explained for Financial Control

Imagine your bank account balance hitting zero at the end of every month – not because you've spent it all frivolously, but because every single dollar has been assigned a job. That's the essence of Zero-Based Budgeting (ZBB). With ZBB, you allocate every dollar of your income to a specific category: expenses, savings, debt repayment, or investments. The goal is for your income minus your expenses (including savings and debt payments) to equal zero. It's like giving every dollar a name and a mission.

How Zero Based Budgeting Works Step by Step Implementation

Implementing ZBB involves a few key steps:

- Calculate Your Monthly Income: Start by figuring out exactly how much money you expect to bring in after taxes each month. This is your starting point.

- List All Your Expenses: This is where you get granular. Categorize everything: rent/mortgage, utilities, groceries, transportation, insurance, subscriptions, entertainment, dining out, personal care, and so on. Don't forget irregular expenses like annual subscriptions or car maintenance – you'll need to set aside money for these too.

- Assign Every Dollar a Job: This is the core of ZBB. Go through your income and allocate funds to each expense category until your income minus your allocated expenses equals zero. If you have money left over, assign it to savings, debt repayment, or a specific financial goal. If you're over budget, you need to adjust your allocations until it balances out.

- Track and Adjust: Throughout the month, track your spending diligently. At the end of the month, review your budget. Did you stick to it? Where did you overspend or underspend? Adjust your categories for the next month based on your actual spending habits.

Pros and Cons of Zero Based Budgeting Detailed Analysis

Pros of ZBB:

- Maximum Financial Awareness: You know exactly where every dollar is going, leading to incredible clarity about your spending habits.

- Prevents Overspending: Because every dollar has a job, there's less room for impulse purchases or 'mystery' spending.

- Accelerates Financial Goals: By intentionally allocating funds to savings or debt, you can reach your goals much faster.

- Highly Adaptable: You create a new budget each month, allowing you to easily adjust for changing income or expenses.

- Empowering: It gives you a strong sense of control over your money, reducing financial anxiety.

Cons of ZBB:

- Time-Consuming: It requires a significant time commitment, especially when you're first starting out, to categorize and track everything.

- Can Be Restrictive: Some people find the strict allocation to be too rigid, leading to budget fatigue.

- Requires Discipline: If you're not diligent with tracking, the system can fall apart quickly.

- Estimating Variable Expenses: It can be challenging to accurately estimate variable expenses like groceries or entertainment each month.

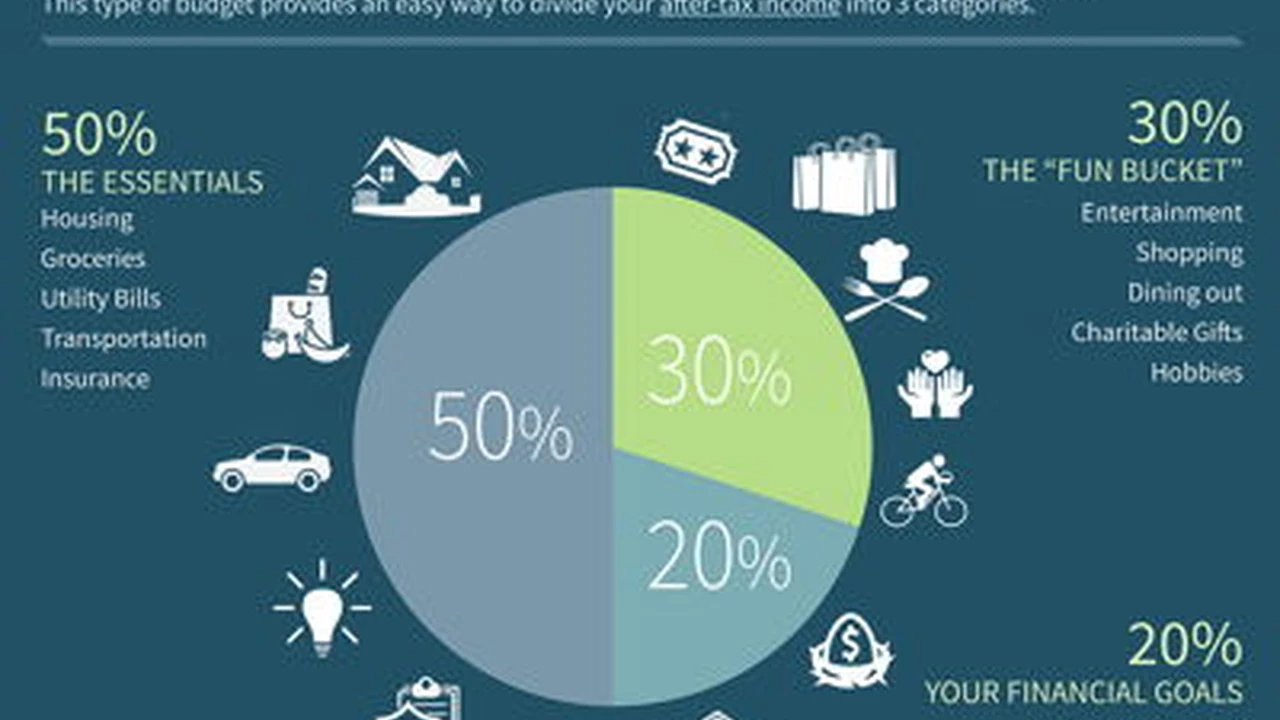

What is the 50 30 20 Rule Simplified Budgeting for Everyone

The 50/30/20 Rule, popularized by Senator Elizabeth Warren, is a much simpler, more generalized budgeting framework. Instead of assigning every dollar, it divides your after-tax income into three broad categories:

- 50% for Needs: These are your essential expenses – things you absolutely cannot live without. Think housing (rent/mortgage), utilities, groceries, transportation, insurance, and minimum debt payments.

- 30% for Wants: These are the things that improve your quality of life but aren't strictly necessary. This includes dining out, entertainment, hobbies, vacations, shopping for non-essentials, and subscriptions.

- 20% for Savings and Debt Repayment: This portion is dedicated to building your financial future. It covers contributions to your emergency fund, retirement accounts (401k, IRA), investments, and any extra payments towards debt beyond the minimum.

How the 50 30 20 Rule Works Easy Application Steps

Applying the 50/30/20 Rule is straightforward:

- Calculate Your After-Tax Income: Just like with ZBB, start with your net income.

- Allocate Percentages: Multiply your income by 0.50 for needs, 0.30 for wants, and 0.20 for savings/debt.

- Categorize Your Spending: Review your current spending and see if it aligns with these percentages. If your 'wants' are eating into your 'needs' or 'savings,' you'll need to make adjustments.

- Monitor and Adjust: While less granular than ZBB, it's still important to periodically check your spending to ensure you're staying within your allocated percentages.

Pros and Cons of the 50 30 20 Rule Quick Overview

Pros of 50/30/20 Rule:

- Simplicity: It's incredibly easy to understand and implement, making it great for budgeting beginners.

- Less Time-Consuming: You don't need to track every single transaction, just ensure your broad categories align.

- Flexibility: It allows for more flexibility within the 'wants' category, which can prevent budget burnout.

- Good Starting Point: An excellent framework for those new to budgeting or who prefer a less rigid approach.

Cons of 50/30/20 Rule:

- Less Granular Control: You might not know exactly where every dollar is going, potentially leading to some 'leakage.'

- May Not Fit All Incomes: For very low or very high incomes, the percentages might need significant adjustment. For example, someone in a high cost of living area might find 50% for needs insufficient.

- Defining Needs vs Wants: Sometimes, the line between a 'need' and a 'want' can be blurry, leading to miscategorization.

- Slower Goal Achievement: While it encourages saving, it might not push you to reach aggressive financial goals as quickly as ZBB.

Zero Based Budgeting vs 50 30 20 Rule A Direct Comparison for Financial Planning

Let's put them side-by-side to highlight their key differences:

| Feature | Zero-Based Budgeting (ZBB) | 50/30/20 Rule |

|---|---|---|

| Granularity | Highly detailed; every dollar assigned. | Broad categories; percentages for needs, wants, savings. |

| Complexity | More complex, requires diligent tracking. | Simple, easy to understand and implement. |

| Time Commitment | High, especially initially and for monthly review. | Low to moderate, less frequent detailed tracking. |

| Flexibility | High monthly adaptability, but strict within the month. | More flexible within categories, less monthly adjustment. |

| Financial Awareness | Maximum awareness of all spending. | Good general awareness, but less detail. |

| Goal Acceleration | Excellent for aggressive goal achievement. | Good for consistent saving, but less aggressive. |

| Best For | Those who want complete control, aggressive savers, debt repayment. | Budgeting beginners, those who prefer simplicity, general financial health. |

Choosing Your Budgeting Method Tailoring to Your Financial Situation

So, how do you decide? It really boils down to your personality, financial goals, and how much time you're willing to dedicate to budgeting.

When Zero Based Budgeting is Your Best Fit Aggressive Financial Goals

ZBB is ideal if:

- You're serious about paying off a significant amount of debt quickly.

- You want to save aggressively for a specific goal (e.g., a down payment, a large vacation, early retirement).

- You've struggled with overspending and need strict accountability.

- You enjoy the process of detailed financial planning and tracking.

- Your income fluctuates, and you need to re-evaluate your budget each month.

When the 50 30 20 Rule is Ideal Simple and Sustainable Budgeting

The 50/30/20 Rule is a great choice if:

- You're new to budgeting and want a simple, easy-to-follow framework.

- You prefer a less restrictive approach that allows for some spontaneity.

- Your income is relatively stable, and your expenses don't fluctuate wildly.

- You're looking for a sustainable long-term budgeting method without too much daily effort.

- You want a good balance between enjoying your money now and saving for the future.

Hybrid Budgeting Approaches Combining the Best of Both Worlds

Who says you have to pick just one? Many people find success by combining elements of both methods. For instance, you could use the 50/30/20 Rule as your overarching framework but apply ZBB principles to specific categories where you tend to overspend (like dining out or entertainment). This gives you the simplicity of the 50/30/20 Rule with the targeted control of ZBB where you need it most.

Recommended Budgeting Tools and Apps for US and Southeast Asia Markets

No matter which method you choose, technology can make your budgeting journey much smoother. Here are some top tools, with a focus on their applicability in the US and Southeast Asian markets, along with their typical pricing and use cases.

For Zero Based Budgeting Enthusiasts Detailed Tracking Solutions

These tools are built for the meticulous tracker, perfect for ZBB.

1. You Need A Budget YNAB The Gold Standard for ZBB

Description: YNAB is arguably the most famous zero-based budgeting app. It's built around the four rules of YNAB: Give Every Dollar a Job, Embrace Your True Expenses, Roll With the Punches, and Age Your Money. It forces you to be proactive with your money, planning every dollar before you spend it. It connects to your bank accounts for easy import of transactions, but the core philosophy is manual allocation.

Use Case: Ideal for individuals or couples who are serious about gaining complete control over their finances, paying off debt, or saving aggressively. It requires commitment but delivers powerful results.

Pricing: Approximately $14.99/month or $99/year (USD). They often offer a free trial.

Availability: Globally accessible, with bank connections primarily strong in the US, Canada, and some European countries. Users in Southeast Asia can still use it effectively by manually importing transactions or using its manual entry features.

Comparison: More hands-on and philosophical than other apps. Its strength lies in its methodology, which truly teaches you how to budget, rather than just track.

2. Actual Budget Open Source and Privacy Focused ZBB

Description: Actual Budget is an open-source, self-hosted budgeting app that also follows the zero-based budgeting philosophy. It offers robust features for categorizing, tracking, and reporting, with the added benefit of complete data privacy since you host it yourself. It's a bit more technical to set up but offers unparalleled control.

Use Case: Best for tech-savvy individuals or those with strong privacy concerns who want a powerful ZBB tool without subscription fees or cloud storage of their financial data. It's also great for developers who want to customize their budgeting experience.

Pricing: Free (open source), but may incur costs for hosting if you don't have a server already (e.g., a small VPS might cost $5-10/month).

Availability: Global, as it's self-hosted. Bank connections are community-driven and might require more setup for specific regions, especially in Southeast Asia.

Comparison: Offers similar ZBB functionality to YNAB but with a focus on open-source principles and self-hosting. Less user-friendly for beginners due to setup complexity.

For 50 30 20 Rule Adherents Simple Tracking Solutions

These tools are great for a more hands-off, percentage-based approach.

1. Mint Free Financial Tracking and Budgeting

Description: Mint is a popular free personal finance app that connects to all your bank accounts, credit cards, loans, and investments. It automatically categorizes your transactions and allows you to set budgets based on categories. While not strictly 50/30/20, its budgeting features can easily be adapted to this rule by setting category limits that align with your percentages.

Use Case: Excellent for anyone looking for a free, automated way to track their spending, monitor their net worth, and get a general overview of their financial health. Good for those who want to see if they're roughly adhering to the 50/30/20 rule without manual input.

Pricing: Free (ad-supported).

Availability: Primarily US and Canada. Limited functionality or bank connectivity in Southeast Asia.

Comparison: More focused on aggregation and automated tracking than proactive budgeting. Great for a quick snapshot but less about intentional dollar allocation.

2. PocketGuard Smart Budgeting and Spending Tracker

Description: PocketGuard aims to simplify budgeting by telling you 'how much you can spend' after accounting for bills, goals, and savings. It connects to your accounts and automatically categorizes transactions. You can set up custom budgets and track your spending against them, making it easy to see if you're staying within your 50/30/20 allocations.

Use Case: Ideal for individuals who want a clear, at-a-glance view of their 'safe to spend' money. It's less about detailed ZBB and more about ensuring you don't overspend in your 'wants' category while covering 'needs' and 'savings.'

Pricing: Free for basic features; PocketGuard Plus is $7.99/month or $79.99/year (USD) for advanced features like debt payoff plans and custom categories.

Availability: Primarily US and Canada. Limited bank connectivity in Southeast Asia.

Comparison: Focuses on simplicity and 'spendable' money. Good for those who want a quick check on their budget without deep dives.

Tools with Strong Southeast Asian Presence and Adaptability

While many global apps exist, local solutions often offer better bank integration and localized features.

1. Spendee Budget and Expense Tracker

Description: Spendee is a visually appealing budgeting app that allows you to connect bank accounts (including many in Southeast Asia), track cash expenses, and create custom budgets. It supports multiple currencies and offers a clear overview of your income and expenses. You can easily set up budgets based on the 50/30/20 rule or create more detailed categories for a ZBB-like approach.

Use Case: Great for individuals and families who want a flexible budgeting tool with good bank integration across various regions, including parts of Southeast Asia. It's versatile enough for both simple and more detailed budgeting.

Pricing: Free for manual entry; Premium is $2.24/month or $14.99/year (USD) for bank connections and unlimited budgets; Plus is $1.67/month or $11.99/year (USD) for multiple wallets and shared budgets.

Availability: Global, with strong bank integration in many European countries, the US, and a growing presence in Southeast Asia (e.g., Singapore, Malaysia, Indonesia, Philippines, Thailand).

Comparison: Offers a good balance of automation and customization, making it adaptable to both ZBB and 50/30/20. Stronger international bank support than Mint or PocketGuard.

2. Wallet by BudgetBakers Personal Finance Manager

Description: Wallet is another robust personal finance manager that supports bank synchronization globally, including a significant number of banks in Southeast Asia. It allows for detailed expense tracking, budget creation, and financial planning. You can set up recurring transactions, track debts, and analyze your spending habits with various reports. It's flexible enough to support both ZBB principles (by meticulously categorizing and assigning funds) and the 50/30/20 rule (by setting percentage-based budgets).

Use Case: Suitable for users who need comprehensive financial management, including multi-currency support and extensive bank connectivity in diverse regions. It's powerful for those who want to track every aspect of their finances.

Pricing: Free for basic features; Premium is $4.99/month or $34.99/year (USD) for unlimited bank connections, advanced reports, and shared wallets.

Availability: Global, with excellent bank integration in the US, Europe, and many countries in Southeast Asia (e.g., Singapore, Malaysia, Indonesia, Philippines, Vietnam, Thailand).

Comparison: Very comprehensive, offering more features than just budgeting. Its global bank support is a significant advantage for users outside the US.

3. Manual Spreadsheet Budgeting Google Sheets or Excel

Description: Sometimes, the best tool is the one you build yourself. A simple spreadsheet (Google Sheets or Excel) can be incredibly powerful for both ZBB and the 50/30/20 Rule. You can customize it exactly to your needs, create your own categories, and track everything manually. There are many free templates available online that you can adapt.

Use Case: Perfect for those who prefer a hands-on approach, want complete customization, or are wary of connecting their bank accounts to third-party apps. It's also a great free option.

Pricing: Free (if you already have Excel or use Google Sheets).

Availability: Universal.

Comparison: Offers ultimate flexibility and privacy but requires the most manual effort. No automation, but complete control.

Final Thoughts on Budgeting Strategies Your Financial Journey

Ultimately, the 'best' budgeting method is the one you'll stick with. Zero-Based Budgeting offers unparalleled control and can accelerate your financial goals, but it demands discipline and time. The 50/30/20 Rule provides a simpler, more flexible framework that's easier to maintain long-term. Don't be afraid to experiment, combine elements, and adjust as your financial situation and goals evolve. The most important thing is to start budgeting today and take control of your money. Happy budgeting!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)