Comparing Unit Trust Funds for Beginners in Malaysia

An overview and comparison of user-friendly unit trust funds in Malaysia suitable for new investors seeking diversification.

An overview and comparison of user-friendly unit trust funds in Malaysia suitable for new investors seeking diversification.

Comparing Unit Trust Funds for Beginners in Malaysia

Hey there, aspiring Malaysian investor! So, you've heard about unit trust funds and are wondering if they're the right starting point for your investment journey. You're in the right place! Unit trust funds are a fantastic way for beginners to dip their toes into the investment world without needing to be a stock market guru. They offer diversification, professional management, and accessibility, making them a popular choice for many Malaysians looking to grow their wealth.

But with so many options out there, how do you choose? It can feel a bit overwhelming, right? Don't worry, we're going to break down what unit trust funds are, why they're great for beginners, and compare some popular options available in Malaysia. We'll even look at specific products, their typical use cases, and what you might expect in terms of costs. Let's get started!

What are Unit Trust Funds and Why Invest in Malaysia?

Think of a unit trust fund as a big pot of money where many investors pool their funds. This collective money is then managed by professional fund managers who invest it across a diversified portfolio of assets like stocks, bonds, properties, and other securities. When you invest in a unit trust, you're essentially buying 'units' of this fund. The value of your units goes up or down depending on the performance of the underlying investments.

Why are they so good for beginners, especially here in Malaysia? Well, for starters:

- Professional Management: You don't need to spend hours researching individual stocks or bonds. The experts do it for you.

- Diversification: Your money is spread across many different assets, reducing the risk compared to investing in just one or two stocks. This is super important for new investors!

- Affordability: You can often start with a relatively small amount, making it accessible to almost everyone.

- Liquidity: You can usually buy and sell your units fairly easily, though redemption periods can vary.

- Accessibility: Many banks, financial advisors, and online platforms offer unit trust funds, making them easy to find and invest in.

Investing in Malaysia specifically offers unique opportunities, given our growing economy and diverse market. Plus, many local funds are tailored to the Malaysian market, offering exposure to local companies and industries.

Types of Unit Trust Funds for Malaysian Investors

Before we dive into specific products, it's good to know the main types of unit trust funds you'll encounter. Each has a different risk profile and investment objective:

Equity Funds Investing in Malaysian Stocks

These funds primarily invest in stocks (equities) of companies. They generally offer higher potential returns but also come with higher risk. If you're comfortable with some volatility and have a longer investment horizon (say, 5+ years), equity funds can be a great growth engine for your portfolio.

Bond Funds Fixed Income Opportunities in Malaysia

Bond funds invest in fixed-income securities like government bonds and corporate bonds. They are generally less volatile than equity funds and are often seen as a way to preserve capital and generate steady income. They're a good option if you're more risk-averse or nearing retirement.

Mixed Asset Funds Balanced Portfolios for Malaysian Beginners

As the name suggests, these funds invest in a mix of equities, bonds, and sometimes other assets. They aim to provide a balance between growth and stability. This type of fund is often recommended for beginners as it automatically diversifies across asset classes, reducing the need for you to manage that balance yourself.

Money Market Funds Short Term Investments in Malaysia

These are the lowest-risk unit trust funds, investing in highly liquid, short-term debt instruments. They're often used for parking cash you might need in the near future, as they offer slightly better returns than a typical savings account without much risk. Don't expect huge returns, but they're great for stability.

Islamic Funds Shariah Compliant Investing in Malaysia

For those who prefer Shariah-compliant investments, Islamic unit trust funds adhere to Islamic principles, avoiding investments in industries like alcohol, gambling, or conventional banking. They can be equity, bond, or mixed-asset funds, just managed according to specific ethical guidelines.

Popular Unit Trust Providers and Their Offerings in Malaysia

Malaysia has a robust unit trust industry with several reputable fund houses. Here are a few prominent ones and some examples of their beginner-friendly funds. Remember, these are examples, and you should always do your own research and consult with a financial advisor.

Public Mutual Funds for Malaysian Investors

Public Mutual is one of the largest and most well-known unit trust companies in Malaysia. They have a vast array of funds catering to different risk appetites and investment goals. They are known for their extensive network of agents.

- Product Example: Public Far-East Select Fund

- Type: Equity Fund (regional focus)

- Use Case: For investors seeking capital appreciation by investing in a diversified portfolio of equities in the Far-East region (including Malaysia). Suitable for those with a medium to long-term investment horizon and a higher risk tolerance.

- Typical Minimum Investment: RM1,000 (initial), RM100 (subsequent)

- Sales Charge: Typically 5.00% of the investment amount.

- Annual Management Fee: Around 1.50% per annum.

- Why it's good for beginners: Offers regional diversification beyond just Malaysia, managed by experienced professionals.

- Product Example: Public Islamic Bond Fund

- Type: Islamic Bond Fund

- Use Case: For investors seeking regular income and capital preservation through Shariah-compliant fixed-income securities. Suitable for those with a low to medium risk tolerance and a medium-term investment horizon.

- Typical Minimum Investment: RM1,000 (initial), RM100 (subsequent)

- Sales Charge: Typically 0.50% of the investment amount.

- Annual Management Fee: Around 0.50% per annum.

- Why it's good for beginners: Lower risk, provides stable income, and is Shariah-compliant.

Eastspring Investments Diversified Funds for Malaysia

Eastspring Investments is another major player, offering a wide range of funds with a strong focus on Asian markets. They are known for their research capabilities.

- Product Example: Eastspring Investments Small-Cap Fund

- Type: Equity Fund (small-cap focus)

- Use Case: For investors looking for higher growth potential by investing in smaller, growing companies in Malaysia. This comes with higher risk and is suitable for aggressive investors with a long-term horizon.

- Typical Minimum Investment: RM1,000 (initial), RM100 (subsequent)

- Sales Charge: Up to 5.50% of the investment amount.

- Annual Management Fee: Around 1.80% per annum.

- Why it's good for beginners (with higher risk tolerance): Offers exposure to a high-growth segment of the market, professionally managed.

- Product Example: Eastspring Investments Income Fund

- Type: Bond Fund

- Use Case: Aims to provide a steady stream of income and capital preservation by investing in a diversified portfolio of fixed-income securities. Suitable for conservative investors.

- Typical Minimum Investment: RM1,000 (initial), RM100 (subsequent)

- Sales Charge: Up to 3.00% of the investment amount.

- Annual Management Fee: Around 0.80% per annum.

- Why it's good for beginners: Lower risk, focuses on income generation, good for portfolio stability.

Principal Asset Management Global and Local Funds in Malaysia

Principal Asset Management (formerly CIMB-Principal Asset Management) offers a comprehensive suite of investment solutions, including unit trusts, catering to both individual and institutional investors.

- Product Example: Principal Asia Pacific Dynamic Income Fund

- Type: Mixed Asset Fund (regional focus)

- Use Case: For investors seeking a balance of income and capital growth by investing in a diversified portfolio of equities and fixed-income securities across the Asia Pacific region. Good for moderate risk investors.

- Typical Minimum Investment: RM1,000 (initial), RM100 (subsequent)

- Sales Charge: Up to 5.50% of the investment amount.

- Annual Management Fee: Around 1.80% per annum.

- Why it's good for beginners: Offers diversification across asset classes and regions, professionally managed for balanced returns.

- Product Example: Principal Islamic Money Market Fund

- Type: Islamic Money Market Fund

- Use Case: For investors looking for a low-risk, highly liquid investment option for short-term cash management, adhering to Shariah principles.

- Typical Minimum Investment: RM1,000 (initial), RM100 (subsequent)

- Sales Charge: Typically 0.00% (no sales charge).

- Annual Management Fee: Around 0.25% per annum.

- Why it's good for beginners: Extremely low risk, good for parking emergency funds or short-term savings.

Kenanga Investors Innovative Funds for Malaysian Growth

Kenanga Investors is known for its innovative products and strong performance in certain categories, particularly in equity funds.

- Product Example: Kenanga Growth Fund

- Type: Equity Fund (Malaysian focus)

- Use Case: Aims for capital growth by investing primarily in Malaysian equities with strong growth potential. Suitable for investors with a higher risk tolerance and a long-term investment horizon.

- Typical Minimum Investment: RM1,000 (initial), RM100 (subsequent)

- Sales Charge: Up to 5.50% of the investment amount.

- Annual Management Fee: Around 1.80% per annum.

- Why it's good for beginners (with higher risk tolerance): Focuses on growth, managed by a reputable fund house.

Understanding the Costs of Unit Trust Funds in Malaysia

Investing isn't free, and unit trust funds come with certain fees. It's crucial to understand these as they can impact your overall returns. Here are the main ones:

Sales Charge Initial Investment Fees in Malaysia

This is a one-time fee you pay when you buy units. It's usually a percentage of your investment amount. For equity funds, it can be as high as 5-6%, while bond funds or money market funds might have lower or even zero sales charges. Some platforms offer discounted sales charges, so always compare!

Annual Management Fee Ongoing Fund Management Costs

This is an annual fee charged by the fund manager for their services. It's expressed as a percentage of the fund's Net Asset Value (NAV) and is deducted directly from the fund's assets. Equity funds typically have higher management fees (1.5-2.0%) than bond funds (0.5-1.0%).

Trustee Fee Fund Oversight Charges in Malaysia

A small annual fee (usually 0.05-0.10%) paid to the trustee who holds the fund's assets on behalf of investors, ensuring compliance and safeguarding your investments.

Redemption Fee Exit Fees for Malaysian Unit Trusts

Some funds might charge a fee when you sell your units, especially if you redeem them within a short period (e.g., less than 6 months). Many funds, however, have no redemption fees.

Switching Fee Changing Funds in Malaysia

If you decide to switch your investment from one fund to another within the same fund house, there might be a small switching fee.

How to Choose the Best Unit Trust Fund for You in Malaysia

With all this information, how do you make a decision? Here's a step-by-step guide for beginners:

1. Define Your Financial Goals and Time Horizon in Malaysia

What are you saving for? A down payment on a house? Retirement? Your child's education? When do you need the money? Your goals and time horizon will dictate your risk tolerance. A long-term goal (10+ years) allows you to take on more risk, while a short-term goal (1-3 years) calls for lower-risk investments.

2. Assess Your Risk Tolerance as a Malaysian Investor

How comfortable are you with the value of your investment going up and down? Can you stomach potential losses for higher long-term gains? Be honest with yourself. If market volatility keeps you up at night, stick to lower-risk funds.

3. Research Fund Performance and History in Malaysia

Look at the fund's historical performance over different periods (1-year, 3-year, 5-year, 10-year). While past performance doesn't guarantee future results, it gives you an idea of how the fund has performed in various market conditions. Compare funds within the same category.

4. Compare Fees and Charges for Malaysian Unit Trusts

As discussed, fees eat into your returns. Compare sales charges, management fees, and other costs across different funds and providers. Sometimes, a slightly lower-performing fund with significantly lower fees can outperform a higher-performing fund with high fees over the long run.

5. Read the Fund Prospectus and Product Highlight Sheet in Malaysia

These documents contain all the essential information about the fund, including its investment objectives, strategies, risks, fees, and past performance. Don't skip this step! It's crucial for understanding what you're investing in.

6. Consider Diversification Across Multiple Funds or Asset Classes

Even within unit trusts, you can diversify. Instead of putting all your money into one equity fund, consider a mix of an equity fund and a bond fund, or even a mixed-asset fund. This further spreads your risk.

7. Seek Professional Financial Advice in Malaysia

If you're still unsure, don't hesitate to consult a licensed financial advisor. They can help you assess your financial situation, goals, and risk tolerance, and recommend suitable unit trust funds tailored to your needs. They can also help you navigate the paperwork and ongoing management.

Platforms to Buy Unit Trust Funds in Malaysia

You have several avenues to purchase unit trust funds in Malaysia:

Banks Traditional Unit Trust Distribution Channels

Most major banks in Malaysia (e.g., Maybank, CIMB, Public Bank, RHB) offer unit trust products from various fund houses. You can walk into a branch and speak to a relationship manager.

Financial Advisors Personalized Investment Guidance in Malaysia

Independent financial advisors can offer a wider range of funds from different providers and provide personalized advice based on your financial plan.

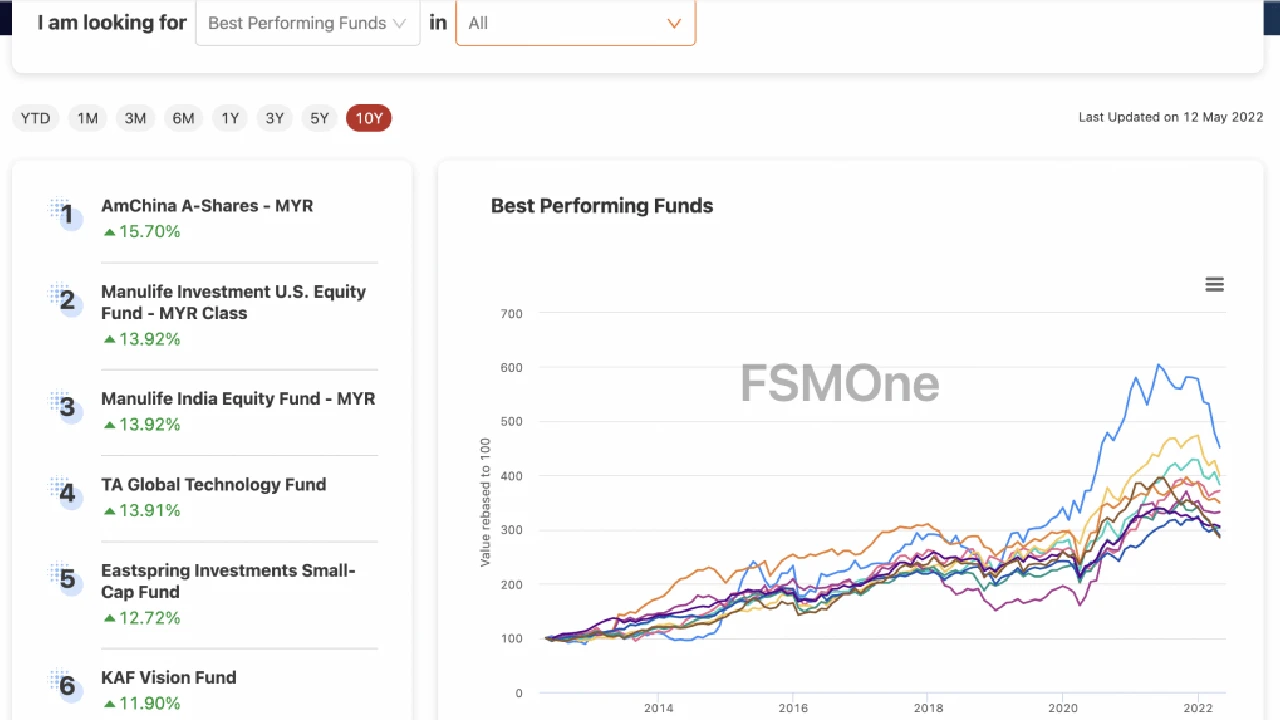

Online Platforms Digital Unit Trust Investment in Malaysia

Platforms like FSMOne (formerly Fundsupermart) and eUnittrust offer a convenient way to buy, sell, and manage unit trusts online, often with lower sales charges compared to traditional channels. These platforms are becoming increasingly popular for tech-savvy investors.

- Platform Example: FSMOne Malaysia

- Use Case: A comprehensive online platform offering a wide selection of unit trust funds from various fund houses, ETFs, and bonds. Ideal for self-directed investors who want to compare and manage their investments online.

- Key Features: Extensive fund selection, research tools, portfolio tracking, often lower sales charges (e.g., 0% to 1.75% for many funds).

- Why it's good for beginners: User-friendly interface, educational resources, and the ability to start with relatively small amounts.

- Platform Example: eUnittrust by IFAST Capital

- Use Case: Another popular online platform for unit trust investments in Malaysia, offering competitive fees and a good range of funds.

- Key Features: Similar to FSMOne, focuses on providing access to a broad spectrum of funds with competitive pricing.

- Why it's good for beginners: Easy to navigate, transparent fee structure, and good for comparing different fund options.

Final Thoughts on Unit Trust Investing for Malaysian Beginners

Unit trust funds are an excellent entry point into investing for beginners in Malaysia. They simplify the investment process by offering professional management, diversification, and accessibility. By understanding the different types of funds, comparing specific products and their associated costs, and choosing the right platform, you can confidently start building your investment portfolio.

Remember, investing is a long-term game. Be patient, stay consistent with your contributions, and regularly review your portfolio to ensure it aligns with your evolving financial goals. Happy investing!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)