Best Cash Back Credit Cards for Everyday Spending in the US

Review the top cash-back credit cards in the US that offer generous rewards for everyday purchases.

Review the top cash-back credit cards in the US that offer generous rewards for everyday purchases.

Best Cash Back Credit Cards for Everyday Spending in the US

Hey there, savvy spender! Are you looking to make your everyday purchases work harder for you? Cash back credit cards are an awesome way to do just that. Instead of just swiping your card and watching your money disappear, imagine getting a percentage of it back in your pocket. Sounds pretty sweet, right? In the US, the market for cash back cards is huge, with tons of options offering different reward structures, bonus categories, and sign-up bonuses. It can be a bit overwhelming to figure out which one is the best fit for your spending habits. But don't worry, we're here to break it all down for you. We'll dive deep into some of the top cash back credit cards, compare their features, discuss their ideal use cases, and even touch on their fees and annual percentage rates (APRs). Our goal is to help you pick the perfect card to maximize your rewards on everything from groceries and gas to dining out and online shopping.

Understanding Cash Back Credit Card Rewards Structures

Before we jump into specific cards, let's quickly chat about how cash back works. Not all cash back cards are created equal, and understanding their reward structures is key to choosing the right one. Generally, you'll encounter a few main types:

Flat Rate Cash Back Cards

These are super straightforward. You earn a fixed percentage of cash back on every single purchase, no matter the category. Think of it as a simple, no-fuss way to get rewards. For example, a card might offer 1.5% or 2% cash back on everything. These are great for people who don't want to track rotating categories or have varied spending habits.

Bonus Category Cash Back Cards

These cards offer higher cash back rates in specific spending categories that often rotate quarterly. For instance, you might earn 5% cash back on groceries and gas one quarter, and then 5% on Amazon and dining the next. The catch? You usually have to activate these bonus categories each quarter, and there's often a spending cap on the higher rate (e.g., 5% back on the first $1,500 spent in bonus categories). After you hit the cap, the rate usually drops to 1%. These cards are fantastic for maximizing rewards if you're organized and willing to keep track of the rotating categories.

Tiered Cash Back Cards

Similar to bonus category cards, but usually with fixed categories that offer different cash back rates. For example, you might get 3% back on dining, 2% on groceries, and 1% on everything else. These are a good middle ground if you want higher rewards in certain areas but prefer consistent categories over rotating ones.

Sign Up Bonuses and Introductory Offers

Many cash back cards come with attractive sign-up bonuses. This is usually a lump sum of cash back (e.g., $200) after you spend a certain amount within the first few months of opening the account (e.g., $500 in 3 months). These can be a great way to kickstart your rewards. Also, keep an eye out for introductory APR offers, which might give you 0% APR on purchases or balance transfers for a set period. This can be useful if you plan to make a large purchase and pay it off over time without incurring interest.

Top Cash Back Credit Cards for Everyday Spending

Alright, let's get to the good stuff! Here are some of the best cash back credit cards currently available in the US, along with their features, ideal users, and some important details.

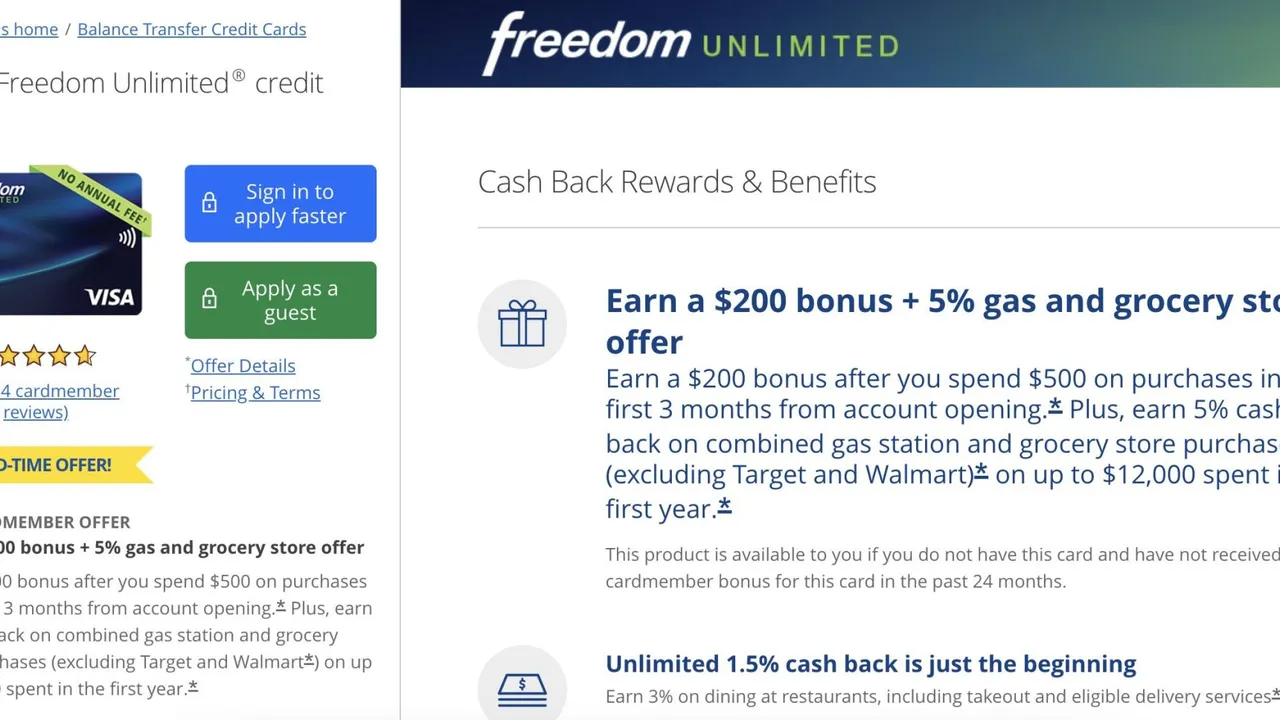

1. Chase Freedom Unlimited

Overview and Key Features

The Chase Freedom Unlimited is a fantastic all-around cash back card that offers a solid rewards rate on every purchase, plus elevated rates in specific categories. It's a Visa card, so it's widely accepted.

- Cash Back Rate: 5% cash back on travel purchased through Chase Ultimate Rewards, 3% cash back on dining at restaurants (including takeout and eligible delivery services), 3% cash back on drugstore purchases, and an unlimited 1.5% cash back on all other purchases.

- Sign-Up Bonus: Often offers a bonus like an extra 1.5% cash back on all purchases (on up to $20,000 spent) in the first year, which means you'd earn 3% on all non-bonus category purchases, 6.5% on travel, 4.5% on dining, and 4.5% on drugstores. This can be a significant boost in your first year.

- Annual Fee: $0

- Introductory APR: Typically offers 0% intro APR on purchases and balance transfers for a period (e.g., 15 months), then a variable APR applies.

- Foreign Transaction Fees: Yes, usually 3%. Not ideal for international travel.

Ideal User and Use Cases

This card is perfect for:

- Everyday Spenders: The 1.5% base rate on all purchases means you're always earning a decent reward, even on things that don't fall into bonus categories.

- Foodies and Health-Conscious Shoppers: The 3% back on dining and drugstores is a great perk if these are significant spending areas for you.

- Travelers (who book through Chase): The 5% on Chase Ultimate Rewards travel can be very lucrative if you frequently book flights or hotels through their portal.

- Those Seeking Simplicity with a Boost: It's more rewarding than a flat 1.5% card but doesn't require tracking rotating categories like some other cards.

- Chase Ecosystem Users: If you also have a Chase Sapphire Preferred or Reserve card, you can combine your Freedom Unlimited points and transfer them to airline or hotel partners for potentially even greater value. This is a huge advantage for maximizing rewards.

Comparison and Pricing

Compared to a flat 2% cash back card, the Freedom Unlimited can offer higher overall rewards if your spending aligns with its bonus categories. For example, if you spend $500 on dining and $500 on drugstores in a month, you'd get $30 back from those categories alone, plus 1.5% on everything else. A flat 2% card would only give you $20 on those same purchases. The $0 annual fee makes it a no-brainer for many. The introductory APR can also be a valuable feature for managing larger purchases without immediate interest.

2. Citi Double Cash Card

Overview and Key Features

The Citi Double Cash Card is renowned for its incredibly simple yet powerful cash back structure. It's a Mastercard, offering broad acceptance.

- Cash Back Rate: Earns an unlimited 2% cash back on every purchase – 1% when you buy and an additional 1% when you pay for those purchases. This effectively means you get 2% back on everything, as long as you pay your bill.

- Sign-Up Bonus: Historically, it hasn't always offered a large cash sign-up bonus, but sometimes has introductory offers like 0% intro APR on balance transfers for a period (e.g., 18 months).

- Annual Fee: $0

- Introductory APR: Often offers 0% intro APR on balance transfers for a period, then a variable APR applies. Purchases usually have a standard variable APR from the start.

- Foreign Transaction Fees: Yes, usually 3%. Not ideal for international travel.

Ideal User and Use Cases

This card is perfect for:

- Simplicity Seekers: If you want maximum cash back without having to think about categories, activation, or spending caps, this is your card.

- High Spenders Across Various Categories: For those who spend a lot across many different categories that don't typically fall into bonus categories (e.g., medical bills, car repairs, general merchandise), the flat 2% is unbeatable.

- Balance Transfer Needs: Its frequent 0% intro APR on balance transfers makes it a strong contender if you're looking to consolidate and pay down existing debt.

- Citi Ecosystem Users: Like Chase, if you have other Citi cards that earn ThankYou Points (like the Citi Premier Card), you can convert your Double Cash rewards into ThankYou Points, potentially increasing their value when transferred to airline partners.

Comparison and Pricing

The Citi Double Cash sets the standard for flat-rate cash back. While cards like the Freedom Unlimited can offer higher rates in specific categories, the Double Cash consistently delivers 2% on everything. This makes it a strong contender for your primary card, especially for purchases that don't earn bonus rewards elsewhere. The $0 annual fee is a major plus. Its lack of a purchase intro APR can be a drawback if you plan to finance new purchases interest-free, but its balance transfer offer is often very competitive.

3. Discover it Cash Back

Overview and Key Features

The Discover it Cash Back card is famous for its rotating 5% cash back categories and its unique first-year bonus. It's a Discover card, which is widely accepted in the US, though sometimes less so internationally.

- Cash Back Rate: 5% cash back on everyday purchases at different places each quarter (up to the quarterly maximum, typically $1,500 spent), when you activate. Plus, unlimited 1% cash back on all other purchases.

- Sign-Up Bonus: Discover matches all the cash back you've earned at the end of your first year, automatically. So, if you earn $300 in cash back, Discover gives you another $300, totaling $600! This is an incredibly generous first-year bonus.

- Annual Fee: $0

- Introductory APR: Typically offers 0% intro APR on purchases and balance transfers for a period (e.g., 14 months), then a variable APR applies.

- Foreign Transaction Fees: None. This is a significant advantage for international travelers, though Discover's international acceptance can be spotty compared to Visa/Mastercard.

Ideal User and Use Cases

This card is perfect for:

- Category Maximizers: If you're diligent about activating categories and aligning your spending, you can earn a lot of cash back. Common categories include gas stations, grocery stores, restaurants, Amazon.com, and wholesale clubs.

- First-Year High Earners: The cash back match in the first year makes this card incredibly rewarding for new cardholders.

- Budget-Conscious Spenders: The 0% intro APR on purchases and balance transfers can be very helpful for managing finances.

- Students or Those Building Credit: Discover is often more forgiving with credit history, and they have excellent customer service.

Comparison and Pricing

The Discover it Cash Back card can offer the highest cash back rates in its bonus categories, often beating out other cards for specific types of spending. However, it requires active management to activate categories and track spending caps. The first-year cash back match is a standout feature that can make it more rewarding than almost any other card in its first year. The $0 annual fee and no foreign transaction fees are also big positives. Its main drawback is the rotating categories, which might not always align with your spending, and Discover's slightly less universal acceptance abroad.

4. Capital One SavorOne Cash Rewards Credit Card

Overview and Key Features

The Capital One SavorOne card is a fantastic choice for those who spend a lot on dining, entertainment, and groceries. It's a Mastercard.

- Cash Back Rate: Unlimited 3% cash back on dining, entertainment, popular streaming services, and at grocery stores (excluding superstores like Walmart and Target). Earn 1% on all other purchases.

- Sign-Up Bonus: Often offers a cash bonus (e.g., $200) after spending a modest amount (e.g., $500) within the first few months.

- Annual Fee: $0

- Introductory APR: Typically offers 0% intro APR on purchases and balance transfers for a period (e.g., 15 months), then a variable APR applies.

- Foreign Transaction Fees: None. This is a great perk for international travelers.

Ideal User and Use Cases

This card is perfect for:

- Foodies and Entertainment Lovers: If you frequently eat out, go to concerts, movies, or subscribe to multiple streaming services, the 3% back in these categories will add up quickly.

- Grocery Shoppers: The 3% back on groceries is a significant benefit for most households.

- Travelers: No foreign transaction fees make it a good card to take abroad, especially for dining and entertainment expenses.

- Those Seeking Consistent Bonus Categories: Unlike rotating category cards, SavorOne's bonus categories are fixed, making it easier to predict and maximize rewards.

Comparison and Pricing

The SavorOne stands out for its strong, consistent bonus categories in popular spending areas. While the base rate is 1%, the 3% on dining, entertainment, streaming, and groceries covers a large portion of many people's budgets. It competes well with cards like the Freedom Unlimited for dining and groceries, but adds entertainment and streaming, which can be a big differentiator. The $0 annual fee and no foreign transaction fees make it a very attractive option. The introductory APR is also a nice bonus for new purchases.

5. Amazon Prime Rewards Visa Signature Card

Overview and Key Features

This card is a must-have for frequent Amazon and Whole Foods Market shoppers who are also Amazon Prime members. It's a Visa Signature card, issued by Chase.

- Cash Back Rate: 5% back at Amazon.com and Whole Foods Market with an eligible Prime membership. 2% back at restaurants, gas stations, and drugstores. 1% back on all other purchases.

- Sign-Up Bonus: Often offers an Amazon.com Gift Card instantly upon approval (e.g., $100-$150).

- Annual Fee: $0 (but requires an Amazon Prime membership, which has an annual fee).

- Introductory APR: No intro APR on purchases or balance transfers; standard variable APR applies.

- Foreign Transaction Fees: None. Excellent for international use.

Ideal User and Use Cases

This card is perfect for:

- Dedicated Amazon Prime Members: If you spend a significant amount on Amazon.com and at Whole Foods, the 5% back is incredibly valuable.

- Everyday Spenders with Specific Habits: The 2% back on dining, gas, and drugstores covers common spending categories.

- Travelers: No foreign transaction fees make it a good companion for international trips.

Comparison and Pricing

For Amazon Prime members, this card offers an unparalleled 5% back on Amazon and Whole Foods, making it the top choice for those specific retailers. No other card consistently offers such a high rate for these popular spending areas. While its other bonus categories (2% on dining, gas, drugstores) are competitive, they might be matched or slightly beaten by other cards. The main 'cost' is the Amazon Prime membership fee, but if you're already a Prime member, this card effectively has no annual fee and offers huge rewards. The instant gift card sign-up bonus is also a nice immediate perk.

6. American Express Blue Cash Preferred Card

Overview and Key Features

The Amex Blue Cash Preferred is a powerhouse for grocery and streaming rewards, though it comes with an annual fee. It's an American Express card.

- Cash Back Rate: 6% cash back at US supermarkets (on up to $6,000 spent per year, then 1%), 6% cash back on select US streaming subscriptions, 3% cash back at US gas stations and on transit, and 1% cash back on all other purchases.

- Sign-Up Bonus: Often offers a statement credit (e.g., $250-$300) after meeting a spending requirement (e.g., $3,000 in 6 months).

- Annual Fee: $0 for the first year, then $95.

- Introductory APR: Typically offers 0% intro APR on purchases for a period (e.g., 12 months), then a variable APR applies.

- Foreign Transaction Fees: Yes, usually 2.7%. Not ideal for international travel.

Ideal User and Use Cases

This card is perfect for:

- Heavy Grocery Spenders: If your household spends a lot on groceries, the 6% cash back (up to $6,000 annually) can easily offset the annual fee and provide significant rewards.

- Streaming Enthusiasts: The 6% back on streaming services is also a top-tier rate.

- Commuters and Road Trippers: The 3% back on gas and transit is a solid perk.

- Those Who Can Maximize Bonus Categories: To make the $95 annual fee worthwhile, you need to spend enough in the 6% and 3% categories to earn more than $95 in rewards.

Comparison and Pricing

The Blue Cash Preferred offers some of the highest cash back rates in its bonus categories, especially for US supermarkets and streaming. No other card consistently offers 6% in these areas. The $95 annual fee is the main consideration. To break even, you'd need to spend about $1,584 annually in the 6% categories ($95 / 0.06). If you spend more than that, the card becomes very rewarding. For example, if you spend $6,000 annually at US supermarkets, you'd get $360 back, easily covering the fee and leaving you with $265 in net rewards. If you don't spend much in these categories, the American Express Blue Cash Everyday Card (which has no annual fee) might be a better fit, offering lower but still good rates (e.g., 3% on US supermarkets, US gas stations, and US online retail purchases).

Factors to Consider When Choosing a Cash Back Card

With so many great options, how do you pick the absolute best one for you? Here are some key factors to weigh:

Your Spending Habits

This is probably the most crucial factor. Do you spend a lot on groceries and gas? Or do you eat out frequently and subscribe to many streaming services? Are your purchases varied, or do you have a few dominant spending categories? If you have consistent high spending in specific areas, a bonus category card like the SavorOne or Blue Cash Preferred might be best. If your spending is all over the map, a flat-rate card like the Citi Double Cash or Chase Freedom Unlimited (with its 1.5% base rate) could be more rewarding.

Annual Fees

Many excellent cash back cards come with no annual fee, which is fantastic because every dollar you earn in cash back is pure profit. However, some cards with annual fees (like the Amex Blue Cash Preferred) can offer significantly higher reward rates that can easily offset the fee if you spend enough in their bonus categories. Always calculate if the rewards you expect to earn will outweigh the annual fee.

Sign-Up Bonuses and Introductory Offers

A generous sign-up bonus can provide a substantial boost to your rewards in the first year. Don't just look at the dollar amount; consider the spending requirement to earn it. Is it achievable within your normal spending? Introductory 0% APR offers can also be very valuable if you plan to make a large purchase or transfer a balance, allowing you to save on interest for a period.

Foreign Transaction Fees

If you travel internationally, foreign transaction fees can quickly eat into your rewards. Many cards charge around 3% on purchases made outside the US. Cards like the Capital One SavorOne, Discover it Cash Back, and Amazon Prime Rewards Visa Signature have no foreign transaction fees, making them better choices for international travel. However, remember to check the acceptance of Discover cards abroad.

Credit Score Requirements

Most of the top cash back cards require good to excellent credit (typically FICO scores of 670 or higher). If your credit score isn't quite there yet, you might need to start with a secured credit card or a card designed for building credit, and then work your way up. Always check the recommended credit score range before applying to avoid a hard inquiry hit on your credit report for a card you're unlikely to get.

Redemption Options

How do you want to receive your cash back? Most cards offer statement credits, direct deposits to a bank account, or gift cards. Some, like Chase and Citi, allow you to convert your cash back into points that can be transferred to airline or hotel partners, potentially increasing their value significantly. If you're interested in travel rewards, this flexibility can be a huge advantage.

Other Card Benefits

Beyond cash back, consider other perks. Do you get purchase protection, extended warranty, rental car insurance, or travel accident insurance? While these aren't direct cash back, they can save you money and provide peace of mind. For example, the Amazon Prime Rewards Visa Signature Card offers travel and purchase protections that can be quite valuable.

Maximizing Your Cash Back Rewards

Getting a great cash back card is just the first step. Here's how to truly maximize your earnings:

Pairing Cards for Optimal Rewards

Many savvy cardholders use a strategy called 'credit card churning' or 'card stacking' (though not necessarily for sign-up bonuses, but for ongoing rewards). This involves using multiple cards, each optimized for different spending categories. For example:

- Use the Amex Blue Cash Preferred for groceries and streaming (6% back).

- Use the Capital One SavorOne for dining and entertainment (3% back).

- Use the Discover it Cash Back for its rotating 5% categories.

- Use the Citi Double Cash or Chase Freedom Unlimited for all other purchases (2% or 1.5% back).

This strategy requires a bit more organization, but it can significantly boost your overall cash back earnings.

Paying Your Bill in Full and On Time

This is non-negotiable. The interest rates on cash back credit cards can be high. If you carry a balance, the interest charges will quickly negate any cash back you earn. Always pay your statement balance in full by the due date to avoid interest and maintain a good credit score. The Citi Double Cash card specifically requires you to pay your bill to get the second 1% cash back, reinforcing this good habit.

Activating Bonus Categories

If you have a card with rotating bonus categories (like the Discover it Cash Back), make sure you activate them each quarter! It's a simple step that many people forget, leaving money on the table.

Utilizing Shopping Portals

Some credit card issuers (like Chase with their Ultimate Rewards portal) and third-party sites offer additional cash back or points when you shop online through their portals. Always check if your favorite retailers are listed before making a purchase.

Monitoring Your Spending

Keep an eye on your spending to ensure you're staying within your budget and maximizing your rewards in the right categories. Many card apps offer spending trackers and category breakdowns.

Potential Downsides and Things to Watch Out For

While cash back cards are great, they're not without their potential pitfalls:

Overspending

The biggest danger with any credit card is overspending. Don't buy things you don't need just to earn cash back. The small percentage you get back is never worth going into debt or buying unnecessary items.

High APRs

After any introductory 0% APR period, the standard variable APRs on cash back cards can be quite high. As mentioned, always pay your balance in full to avoid interest charges.

Annual Fees (if not offset by rewards)

If you choose a card with an annual fee, make sure you're earning enough rewards to justify it. If your spending habits change, or you're not maximizing the bonus categories, a no-annual-fee card might be a better choice.

Foreign Transaction Fees

Be mindful of these if you travel abroad. If your card charges them, consider using a different card that doesn't, or carry some local currency.

Credit Score Impact

Applying for multiple credit cards in a short period can temporarily lower your credit score due to hard inquiries. Only apply for cards you genuinely need and are likely to be approved for. Also, closing old credit cards can sometimes negatively impact your credit utilization ratio and average age of accounts, so think twice before closing a card, especially if it's one of your oldest.

Final Thoughts on Cash Back Credit Cards

Cash back credit cards are a fantastic financial tool when used responsibly. They allow you to get a little something back from your everyday spending, effectively reducing the cost of your purchases. Whether you prefer the simplicity of a flat-rate card like the Citi Double Cash, the targeted rewards of the Capital One SavorOne or Amex Blue Cash Preferred, or the rotating categories of the Discover it Cash Back, there's a card out there that's perfect for your lifestyle. Remember to always prioritize paying your balance in full, understanding the card's terms, and choosing a card that genuinely aligns with your spending habits. By doing so, you can turn your regular expenses into a steady stream of rewards, putting more money back in your pocket.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)